The Subscription Billing module, contract revenue schedules, ASC 606 / IFRS 15 mechanics, deferred revenue, the GL flow from contract inception through recognition, and the configuration decisions that produce an auditable revenue schedule — or require Finance to maintain a parallel spreadsheet for the next three years.

The ASC 606 / IFRS 15 Framework — What the System Must Encode

ASC 606 (US GAAP) and IFRS 15 (international) share a common five-step revenue recognition model. D365 F&O’s Subscription Billing module is designed to operationalize this framework at the contract level — but the accounting judgments that the framework requires must be made by Finance and its auditors before the system can be configured to apply them consistently.

The Five-Step Revenue Recognition Framework — What System Configuration Encodes

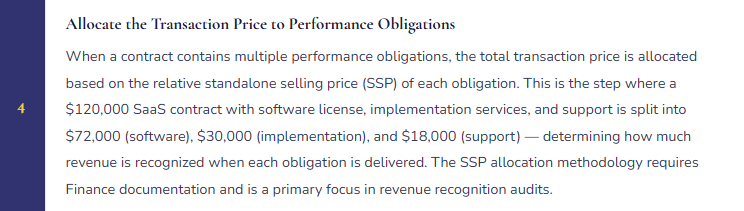

The Subscription Billing Module — Key Components

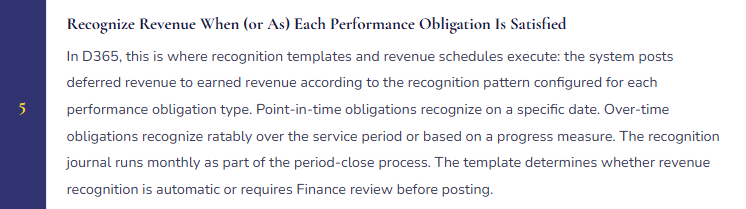

D365 F&O’s Subscription Billing module (introduced in recent release waves to replace the legacy Revenue Recognition feature) manages recurring contracts through three interconnected components: billing schedules, deferral schedules, and revenue allocation.

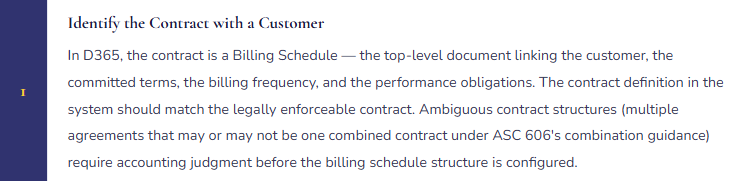

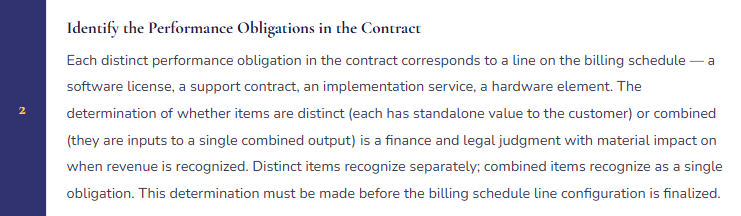

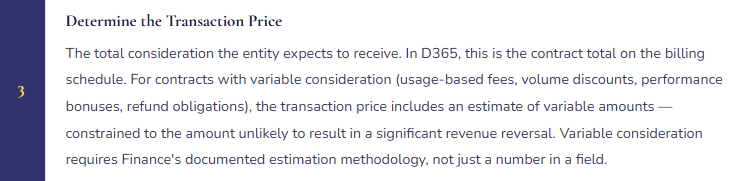

Billing Schedules are the central contract document — they define the customer, the billing items, the billing frequency (monthly, quarterly, annually, usage-based), the contract start and end dates, and the escalation rules for price changes over the contract term. The billing schedule drives invoice generation: when a billing period closes, the billing schedule produces the customer invoice for that period automatically. Billing schedules support pauses, terminations, renewals, and amendments — each with tracked financial impact on the revenue schedule.

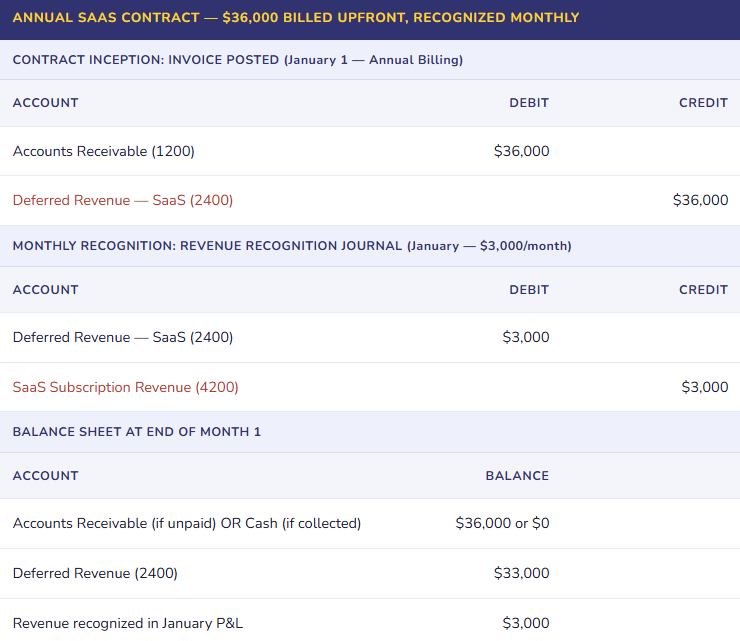

Deferral Schedules manage the timing difference between invoicing and revenue recognition. When a customer is billed upfront for an annual subscription, the full invoiced amount posts to deferred revenue (a liability). The deferral schedule then releases deferred revenue to earned revenue ratably over the subscription period — one-twelfth per month for an annual contract. The deferral schedule is generated at invoice posting and runs automatically each period through the recognition journal.

Revenue Allocation handles multi-element arrangements — contracts with multiple performance obligations at different transaction prices. Finance configures standalone selling prices (SSP) for each item, and the revenue allocation engine distributes the contract transaction price across obligations proportionally to their relative SSPs. The allocated amounts — not the billed amounts — drive the revenue schedule for each obligation.

The GL Flow — From Contract Inception to Revenue Recognized

Transaction Price Allocation — The Configuration That Auditors Look at Hardest

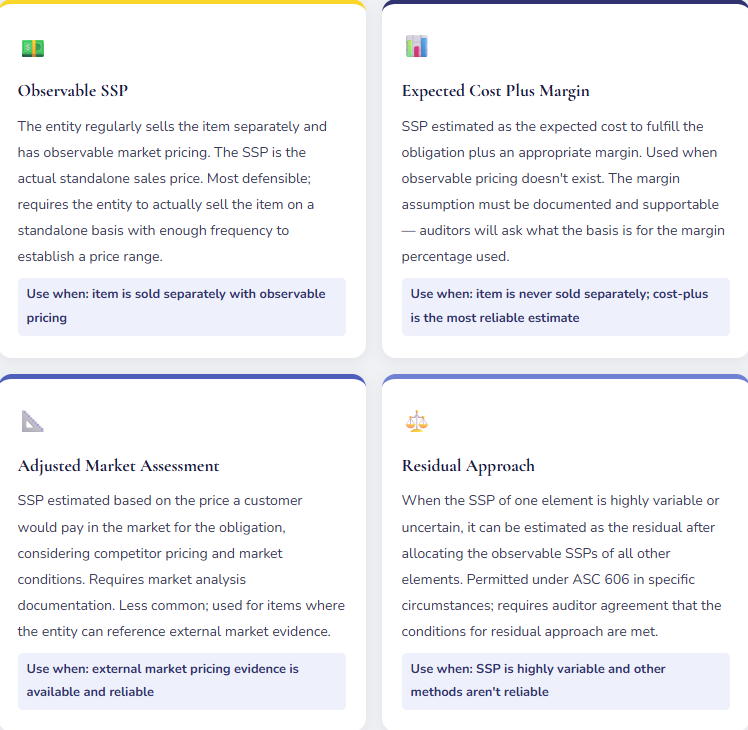

For contracts containing multiple performance obligations, D365’s revenue allocation module distributes the contract transaction price based on the relative standalone selling price (SSP) of each element. The SSP is what the entity would charge a customer for that element if it were sold separately. When an entity sells bundled products or services at a discount, the discount is allocated across obligations proportionally to their SSPs — meaning each element in the bundle is recognized at less than its standalone price.

Contract Modifications — The Accounting Decision That Must Happen at Amendment

Subscription contracts get amended — prices change, scope expands, services are added or removed. Each modification requires a finance judgment about how to account for the change: does the modification represent a new contract (prospective, separate revenue schedule), a modification of the existing contract (cumulative catch-up adjustment), or a termination and replacement (full reset)? ASC 606 provides the framework; the judgment must be applied consistently and documented at the time of each modification. D365 supports contract modifications in Billing Schedules, but the system will apply whichever accounting approach Finance configures — it will not make the judgment for you.

Five Mistakes That Produce a Revenue Recognition Implementation That Doesn’t Survive Audit

⚠️ Revenue Recognition Configured Without Auditor Involvement — The System Encodes Unchallenged Assumptions

- The implementation team configures revenue recognition based on Finance’s description of how revenue works. Nobody involves the external auditor in the design sessions. The system goes live. The first year-end audit involves a detailed review of the revenue recognition methodology. The auditor identifies that the implementation service element in multi-element contracts has been treated as non-distinct and bundled with the software license, when the auditor’s view is that implementation is a distinct performance obligation. Restatement of twelve months of revenue recognition is required — separating implementation revenue from software license revenue and adjusting the recognition timing for each. The revenue recognized and the deferred revenue balance are both materially restated.

- Fix: External auditors must be in the design sessions for ASC 606 / IFRS 15 revenue recognition configuration. Not for information sharing after the configuration is done — in the sessions where accounting judgments are made. The questions that require auditor input: which elements are distinct performance obligations? What is the SSP for each? Which obligations are satisfied over time versus at a point in time? What is the recognition pattern for each? These are audit-sensitive accounting conclusions that should be documented and agreed before they’re encoded in the system configuration.

⚠️ Recognition Journal Not Run Monthly — Deferred Revenue Balance Doesn’t Move

- The Subscription Billing module is configured correctly. Deferral schedules are generated at invoice posting. But the recognition journal — the monthly process that releases deferred revenue to earned revenue — isn’t in anyone’s period-close checklist. For three months it’s forgotten. The deferred revenue balance is $840,000 higher than it should be because three months of recognition hasn’t run. The income statement is missing $840,000 of revenue that was earned and should have been recognized. When Finance catches it, the correction requires running three months of recognition journal catch-up — three journal entries that hit the income statement simultaneously, creating an unexplained revenue spike in the correction period that leadership and auditors will ask about.

- Fix: The recognition journal is a required period-close step, not optional cleanup. It belongs on the period-close checklist with a specific owner, a specific run date within the close schedule, and a specific review step — Finance should verify that the recognition journal ran and that the posted amounts match the expected monthly recognition for the active deferral schedules. Consider scheduling the recognition journal to run automatically on a defined date each period rather than relying on manual triggering. Automation of a routine, repeatable journal reduces the risk of omission.

⚠️ Deferred Revenue Not Classified Between Current and Long-Term — Balance Sheet Presentation Is Wrong

- All deferred revenue posts to a single Deferred Revenue account (2400) regardless of the expected recognition timing. The balance sheet presents $1.2M of deferred revenue as a single current liability. For contracts with recognition periods extending beyond twelve months, the portion not expected to be recognized within the next twelve months should be classified as long-term deferred revenue — a separate line on the balance sheet. The single-account approach overstates current liabilities, understates long-term liabilities, and misrepresents the timing of the company’s revenue recognition obligations. For a SaaS company with multi-year contracts, this misclassification can be significant enough to affect financial ratio analysis, covenant calculations, and investor presentation.

- Fix: Configure separate deferred revenue accounts — Deferred Revenue Current (2400) and Deferred Revenue Non-Current (2410). The allocation between current and non-current must be calculated at each period close: the portion of active deferral schedules expected to recognize within the next twelve months belongs in current; the remainder belongs in non-current. D365 deferral schedules carry the recognition timeline, so the data is available — it requires a classification step at period close rather than a single lump-sum balance. Auditors will require this classification; build it into the setup rather than manually reclassifying at year-end.

⚠️ Contract Modifications Handled as New Billing Schedules — Prior Period Deferred Revenue Never Cleared

- When customers amend their contracts, the team creates a new billing schedule for the modified terms rather than amending the existing one. The intent is simplicity — starting fresh avoids the complexity of modifying an existing schedule. The result: the original billing schedule’s deferral schedule continues releasing revenue for a contract that has been superseded. The new billing schedule generates its own deferral and recognition. For six months, both schedules run simultaneously — the customer is being recognized as two separate revenue streams when they are one customer with one modified contract. Deferred revenue is overstated by the remaining balance on the superseded original schedule. The correction requires terminating the original schedule (clearing its deferred balance) and adjusting the new schedule’s opening balance for the modification accounting treatment.

- Fix: Contract modifications must go through the modification process in the existing billing schedule — not through creating parallel schedules. Define a modification procedure: Finance is notified of contract amendments before the billing change takes effect, Finance determines the appropriate accounting treatment (separate contract, modification, or termination-and-replacement), and the modification is processed in D365 using the correct treatment. Creating new schedules for every change is the path of least resistance operationally but the path of maximum complexity for revenue recognition accuracy. The short-term convenience isn’t worth the cumulative accounting problem.

⚠️ SSP Documentation Not Maintained — Allocations Have No Defensible Basis After Year Two

- At go-live, Finance established standalone selling prices for each performance obligation based on a pricing analysis and documented the basis. For the first audit, the documentation was adequate. Over the following two years, pricing evolved — list prices changed, discount patterns shifted, new elements were added to the product portfolio. The SSP amounts in D365 were updated periodically based on Finance’s judgment of current pricing, but the documentation wasn’t updated to reflect the revised analysis. By year three, the configured SSPs reflect current pricing but the documentation references a two-year-old analysis that doesn’t match current prices. The auditor asks for the basis of the current SSP for the professional services element. Finance cannot produce current documentation. The auditor treats the allocation methodology as undocumented and requires the company to perform a retrospective SSP analysis for all contracts in the audit period.

- Fix: SSP documentation is not a go-live artifact — it is a living document that must be updated whenever SSPs change. Build the SSP review into the annual accounting policy review cycle: each year, Finance reviews the configured SSPs against current observable pricing, updates the documentation to reflect the current methodology and supporting data, and obtains auditor concurrence before the updated SSPs take effect for new contracts. Treat SSP documentation with the same discipline as other accounting policy memoranda. The schedule for SSP review should be in the Finance calendar, not dependent on someone remembering to do it.

Do This / Don’t Do This

✓ Do This

- Involve external auditors in revenue recognition design sessions — not after configuration, in the sessions

- Document the accounting judgment for each performance obligation determination before configuring billing schedule lines

- Run the recognition journal as a required period-close step with a named owner

- Configure separate current and non-current deferred revenue accounts

- Process contract modifications through the existing billing schedule using the correct modification treatment

- Maintain SSP documentation as a living document — update annually and when pricing changes

- Reconcile the deferred revenue balance in D365 to the schedule of active deferral schedules at every period close

- Obtain auditor agreement on SSP methodology before it takes effect for new contracts

- Schedule the recognition journal to run automatically rather than relying on manual triggering

✗ Don’t Do This

- Configure revenue recognition without external auditor involvement in the design

- Let the recognition journal slip from the period-close checklist — deferred revenue stops moving

- Post all deferred revenue to a single account without current/non-current classification

- Create new billing schedules for contract modifications — process modifications in the existing schedule

- Update SSP amounts in D365 without updating the documentation that supports them

- Treat SSP documentation as a go-live artifact rather than a maintained accounting policy

- Configure revenue recognition without documenting which elements are distinct performance obligations and why

- Use the residual approach for SSP without auditor agreement that the conditions are met

Up Next:

We’ve now covered the full arc from foundational financial setup through manufacturing, tax, expense management, and subscription billing. The series continues with the supply chain execution layer: Advanced Warehouse Management in D365 F&O — directed put-away and pick, license plate tracking, wave and work management, and the finance implications of advanced WMS including inventory accuracy, COGS timing, and the reconciliation controls Finance needs when the warehouse runs on directed work rather than manual transactions.

— Bobbi

D365 Functional Architect · Recovering Controller

Leave a Reply