How BC’s intercompany module automates reciprocal transactions between related entities, the setup sequence Finance must complete before the first intercompany transaction posts, the intercompany reconciliation and elimination process Finance must run before consolidating, and the five intercompany accounting failures that keep Finance teams reconciling related-party balances manually every close when BC was designed to handle it automatically.

What BC’s Intercompany Module Does—The Mechanics Finance Must Understand

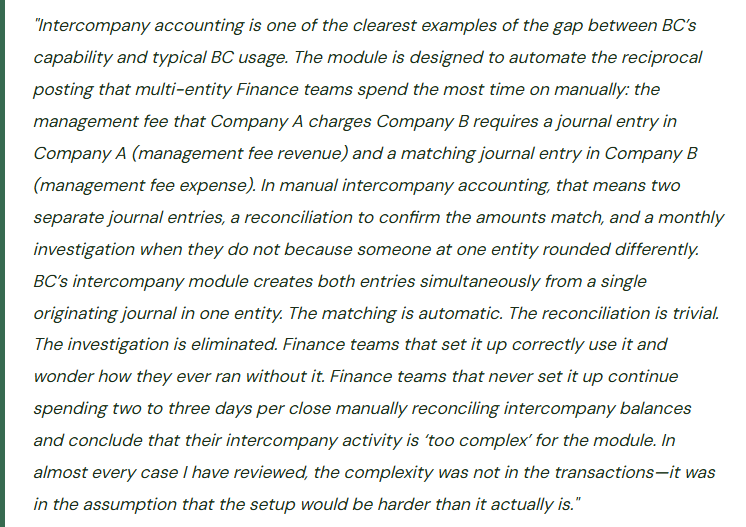

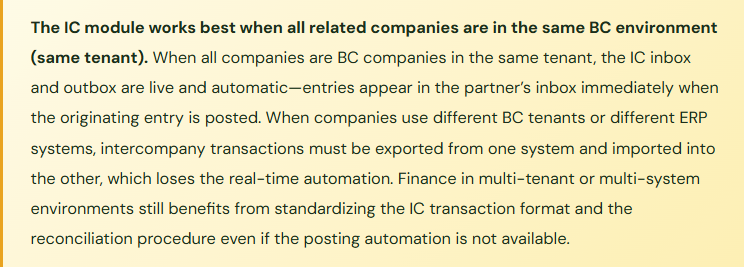

BC’s intercompany (IC) module automates two things: the creation of matching journal entries in a partner entity when an originating entry is posted in the originating entity, and the routing of intercompany transactions through an inbox/outbox system that allows the receiving entity to review and accept or reject incoming intercompany entries before they post to its books.

Each company in the BC intercompany setup has an IC Inbox and an IC Outbox. When Company A posts an intercompany journal entry, BC places the partner entity’s corresponding entry in Company B’s IC Inbox. Company B’s Finance team reviews the inbox entry, confirms it is correct, and accepts it—at which point BC posts the corresponding entry to Company B’s GL. The originating entity’s outbox tracks the status of all sent transactions. The review-and-accept model is the control that gives each entity’s Finance team oversight of transactions posted to their books by another entity. Finance for Company B does not need to trust that Company A entered the correct amount in the correct account—they review the inbox entry before it posts.

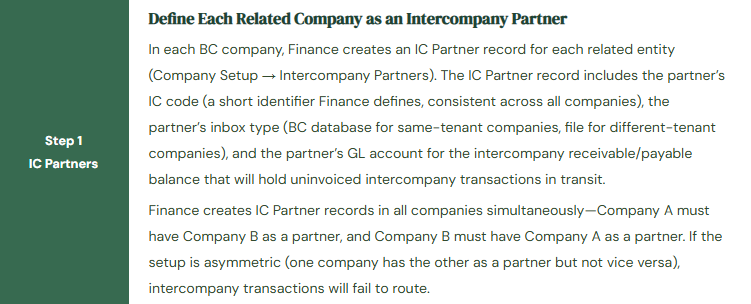

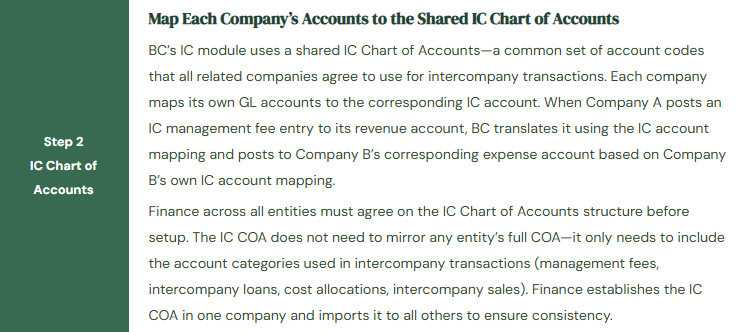

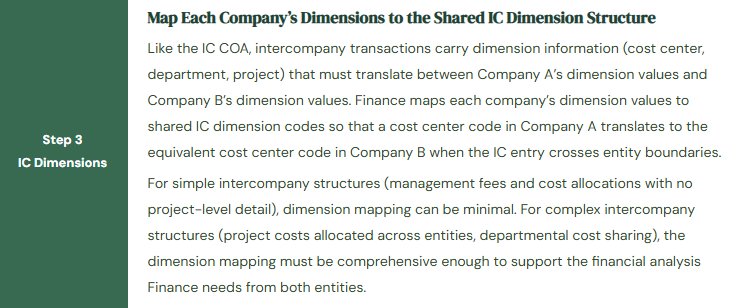

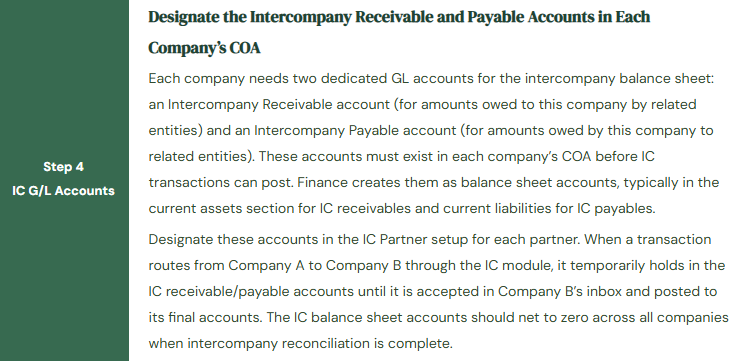

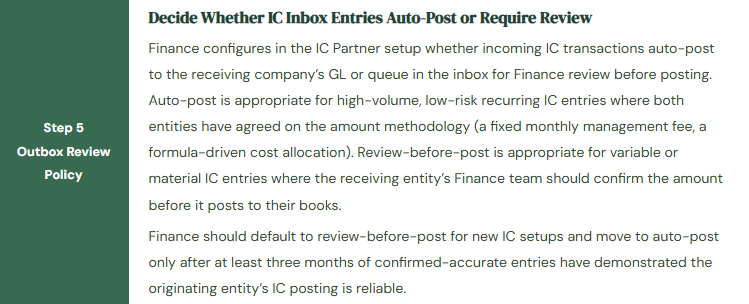

The Intercompany Setup Sequence—Finance Must Complete These Before the First Transaction

Intercompany Setup Sequence—Complete in Order Before Any IC Transaction

The Intercompany Period-End Reconciliation Finance Must Run

Before consolidating or closing any period that includes intercompany activity, Finance must confirm that the intercompany receivable and payable balances across all related entities agree. The IC reconciliation confirms that every IC receivable in one company has a corresponding IC payable in the partner company of equal amount. An IC balance that does not have a matching balance in the partner entity is an outstanding reconciling item that must be explained and resolved before the period closes.

Five Intercompany Accounting Failures That Keep Finance Reconciling Manually

⚠️ IC Module Never Set Up—Two Years of Manual Intercompany Entries Are Inconsistent

A two-entity BC environment (parent company and a wholly owned subsidiary) has been operating for two years without using BC’s IC module. The monthly management fee from the parent to the subsidiary is processed by the parent’s Controller posting a revenue entry in the parent’s BC company and emailing the subsidiary’s bookkeeper to post the corresponding expense in the subsidiary’s BC company. The amounts agree in most months. In seven of the 24 months, there is a small difference between the parent’s revenue entry and the subsidiary’s expense entry due to rounding or data entry variation. The cumulative IC imbalance over 24 months is $1,840. Finance discovered it during the preparation of the group consolidated accounts and spent four hours tracing the discrepancy across 24 months of manual entries.

Fix: The IC module setup for a two-entity structure with a single recurring management fee takes one day. The output is an intercompany transaction that creates both the parent’s revenue entry and the subsidiary’s expense entry simultaneously from a single posting action—no email required, no manual coordination, no rounding discrepancy. Finance should evaluate the IC module setup effort against the monthly manual reconciliation time: if the manual intercompany process takes two hours per month plus four hours per year for the annual discrepancy investigation, the break-even on the one-day setup investment is approximately six months. Finance should complete the IC module setup before the next month-end close, not at some undefined future point when there is more time.

⚠️ IC Partner Setup Incomplete—One-Way Routing Causes Transactions to Fail

Finance sets up Company A as an IC partner in Company B but does not complete the corresponding setup of Company B as a partner in Company A. The setup is asymmetric. When the Finance team at Company A attempts to post an IC journal entry that should route to Company B’s inbox, the transaction fails with a configuration error. Finance escalates to IT, who investigate for half a day before identifying that the IC partner registration is missing from Company A. During the investigation, the IC transaction is held up and the month-end IC reconciliation cannot proceed. The half-day investigation delay pushes the period close by one day.

Fix: IC partner setup must be completed symmetrically across all companies before any IC transaction is posted. Finance creates a setup verification checklist: after configuring IC partners in all companies, Finance sends a test IC journal entry from Company A to Company B and confirms it appears in Company B’s IC inbox. Then Finance sends a test IC journal entry from Company B to Company A and confirms the reverse route works. Only after both directions are confirmed does Finance proceed to the first live IC transaction. The test takes 15 minutes and confirms the setup is bidirectional before any production IC activity depends on it.

⚠️ IC Inbox Entries Accepted Without Review—An Incorrect Amount Posts to the Subsidiary’s Books

Company A posts a quarterly IC cost allocation to Company B. The allocation is formula-driven and usually calculated correctly, but in Q3 the Finance analyst at Company A makes a data entry error in the allocation calculation and overstates Company B’s share by $12,400. Company B is configured for auto-accept on IC inbox entries (Finance set this up during implementation to minimize month-end coordination). The $12,400 overstated allocation posts automatically to Company B’s cost allocation expense account without review. Company B’s Finance team discovers the overstated expense during their budget variance review—three weeks after the close. Correcting it requires a reversing journal in Company B and a corrected IC allocation from Company A, re-routing through the IC module, and re-accepting in Company B’s inbox. Total correction time: four hours, spread across two entities.

Fix: Auto-accept for IC inbox entries should be reserved for fixed-amount recurring transactions where the amount is mechanically determined and verified before posting—a fixed monthly management fee of a specific agreed amount, for example. Variable or formula-driven allocations should require review-before-post so Company B’s Finance team can confirm the amount before it posts to their books. Finance reviews the IC inbox on the same day the originating entity sends the entry—the inbox review is a period-close task, not a background activity. If Company A sends an allocation on Day 2 of the close, Company B reviews and accepts (or returns with a query) on Day 2. The review adds 10 minutes to the close and prevents three-week-delayed corrections.

⚠️ No IC Reconciliation Before Consolidation—Consolidated Balance Sheet Shows IC Imbalances

Finance prepares the annual consolidated accounts. The consolidation process aggregates all BC companies’ balances and the Finance team posts manual elimination journal entries to remove intercompany revenues, expenses, receivables, and payables. After posting the eliminations, the consolidated balance sheet still shows a $34,000 net balance in the IC accounts. Finance investigates and finds that seven intercompany transactions during the year were accepted in the receiving entity’s inbox at amounts that differed from the originating entity’s posted amounts—small differences that accumulated to $34,000 over 12 months of unreconciled IC activity. The reconciliation that would have caught each difference in the month it occurred takes 15 minutes per month. Tracing 12 months of accumulated differences at year-end takes two days and requires the Controller’s direct involvement.

Fix: The IC balance reconciliation is a monthly period-close procedure, not an annual consolidation exercise. Finance runs the IC balance report for all companies at every month-end and confirms IC receivables and payables are in agreement before the period closes. Any difference above a defined tolerance is investigated and resolved in the same close cycle. Monthly discrepancies caught at month-end are typically one or two transactions; annual discrepancies not caught during the year are typically many small transactions that compound into a material investigation. Finance includes the IC reconciliation in the period-close checklist with a specific completion criterion: IC receivable balance in Company A for Company B must agree to IC payable balance in Company B for Company A within $0 before the period is locked in either company.

⚠️ IC Account Mapping Not Updated After COA Change—Six Months of IC Transactions in the Wrong Account

Finance restructures the chart of accounts for all BC companies, splitting the Management Fee Revenue account (GL 4500) into two accounts: Management Fee—IT Services (GL 4510) and Management Fee—Finance Services (GL 4520). Finance updates the COA in all companies. Finance does not update the IC Chart of Accounts mapping or the IC account mappings in the IC partner setup. For six months, all IC management fee transactions continue routing through the IC account that mapped to the old GL 4500. The IC module posts management fee revenue to the old account number, which no longer exists in the COA after the restructure. BC creates entries to an inactive account. The postings succeed (BC does not always prevent posting to inactive accounts depending on the account blocking configuration) but the revenue lands in an inactive account that does not appear on the Management Reporter income statement. Management fee revenue is invisible in all financial reports for six months.

Fix: IC account mapping updates must be included in the COA change procedure alongside all other mapping updates. When any GL account used in intercompany transactions is renamed, split, or deactivated, Finance updates: the IC Chart of Accounts to reflect the new account structure, the IC account mapping for each company to map the new accounts to the correct IC accounts, and any IC transaction templates or recurring IC journal entries that reference the old accounts. Finance adds “Review IC account mappings” to the COA change checklist alongside “Update vendor G/L defaults,” “Update posting groups,” and “Update Financial Report row definitions.” A COA change that affects intercompany accounts requires updates in every company in the IC setup, not just the company where the change was initiated.

Do This / Don’t Do This

Do This

- Complete the IC module setup (IC partners, IC COA, IC dimensions, IC GL accounts) before the first intercompany transaction is needed—not after months of manual entries have accumulated

- Test IC routing in both directions between all company pairs before any production IC activity

- Default to review-before-post for variable IC transactions; reserve auto-accept for fixed-amount recurring entries

- Run the IC balance reconciliation as a monthly period-close procedure before consolidating

- Include IC account mapping review in the COA change procedure—update mappings in all companies simultaneously when accounts change

- Confirm IC receivable and payable balances net to zero in the consolidated view after elimination entries are posted

Don’t Do This

- Continue manual intercompany entries when the IC module is available—the manual process accumulates imbalances that compound over time

- Configure IC partner setup in only one direction—IC routing requires symmetric setup in all company pairs

- Enable auto-accept for all IC inbox entries without distinguishing fixed from variable transactions

- Defer the IC balance reconciliation to the annual consolidation exercise—monthly discrepancies caught at month-end take 15 minutes; annual accumulated discrepancies take days

- Update the COA in one company without updating IC account mappings across all companies in the IC network

- Assume the consolidated balance sheet’s IC accounts are zero after eliminations without explicitly confirming it

Up Next:

Intercompany accounting closes the multi-entity arc. The next post is the one I have been thinking about since Post 1 of this series: A Letter to the Controller Who Just Signed the Implementation Contract—a direct letter to the Finance leader at the beginning of a BC implementation, written from the perspective of someone who has seen every mistake in this series made by smart, capable Finance teams who were given the wrong information or not given enough information at the right moment. Everything this series has covered, distilled into what Finance most needs to hear in the first week of an implementation.

— Bobbi

D365 Functional Architect · Recovering Controller

Leave a Reply