Asset cards, depreciation books, acquisition posting, disposals, the asset register-to-GL reconciliation, and why the decisions made in FA setup determine whether your asset register and your balance sheet agree at year-end.

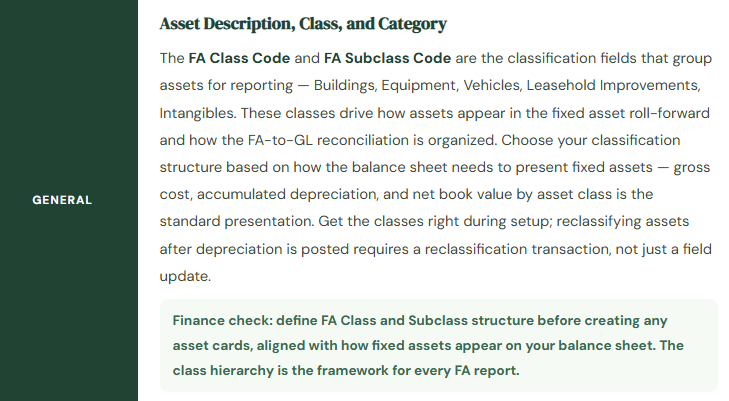

The Fixed Asset Card — What Every Asset Needs Configured

Every physical or intangible asset tracked in BC has a Fixed Asset Card — the master record that holds the asset’s identification, classification, and the depreciation parameters that govern how and when depreciation is calculated. The fields that matter to Finance are spread across several tabs.

Depreciation Books — GAAP, Tax, and Why You Might Need Both

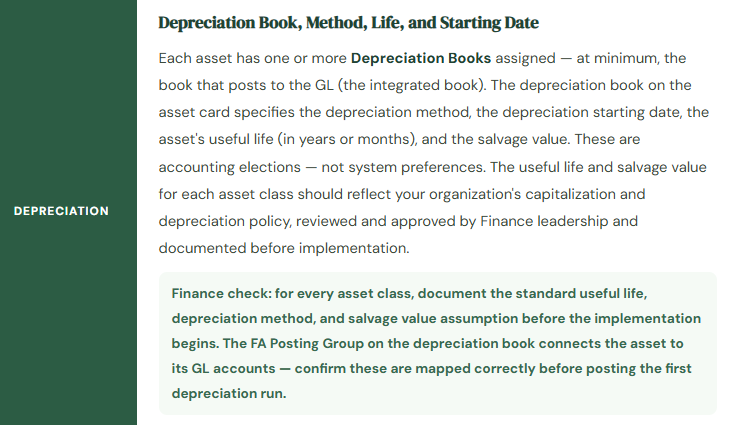

A Depreciation Book in BC is a complete depreciation calculation engine — it maintains its own set of acquisition cost, depreciation taken, and net book value records independently of other books. An asset can have multiple depreciation books, each with its own method, useful life, and posting configuration.

The most common multi-book configuration: one integrated book (posts to the GL, reflects GAAP depreciation for financial reporting) and one non-integrated book (does not post to the GL, used for tax depreciation calculations under MACRS or IRS rules without affecting the financial statements). The tax book gives Finance the information needed for tax return preparation without creating a second set of GL entries that would have to be reversed for financial reporting purposes.

📉 Straight-Line (SL)

- Equal depreciation amount every period for the asset’s useful life. Cost minus salvage value divided by useful life in periods. Produces the most predictable P&L depreciation expense — no acceleration, no year-end surprises. The method most commonly required for GAAP financial reporting of buildings, leasehold improvements, and long-lived assets.

- Best for: buildings, furniture, leasehold improvements, most intangibles. The GAAP default for assets without a compelling reason to accelerate.

📊 Declining Balance (DB)

- A fixed percentage applied to the asset’s remaining book value each period. Produces higher depreciation expense in early years, lower in later years. Reflects the economic reality that many assets (vehicles, equipment) lose value faster in early use. BC supports both straight Declining Balance and Double Declining Balance variants.

- Best for: vehicles, technology equipment, assets where front-loading depreciation reflects actual economic obsolescence. Review whether accelerated depreciation is appropriate under GAAP for your asset class before applying.

📋 Units of Production

- Depreciation calculated based on actual usage — machine hours, miles driven, units produced — rather than time elapsed. Theoretically the most accurate match of expense to economic benefit. In practice, requires reliable usage data for every asset every period, which is the administrative challenge. Well-suited for production equipment where usage data is already tracked.

- Best for: manufacturing equipment with reliable usage tracking, vehicles where odometer readings are maintained, any asset where economic life is genuinely consumption-based rather than time-based.

🔢 Manual

- No automatic depreciation calculation — the Accountant enters depreciation amounts manually period by period. Used for assets with non-standard depreciation schedules, assets being depreciated per a specific amortization table agreed with auditors or regulators, or assets in the final periods of their life where automated calculations don’t produce the correct result.

- Use sparingly. Manual depreciation eliminates the automation benefit of the FA module and requires careful documentation to explain the manual amounts at audit time.

⚡ Sum-of-Years Digits (SYD)

- An accelerated method that produces higher depreciation in early years using the sum-of-the-years as a denominator. Less common than declining balance but available in BC. More complex to explain at audit than straight-line or declining balance, and rarely required by GAAP except for specific asset classes.

- Use only when specifically required by GAAP for an asset class, or when agreed with auditors as the appropriate method for a particular asset type. The complexity of explanation should be weighed against the economic accuracy benefit.

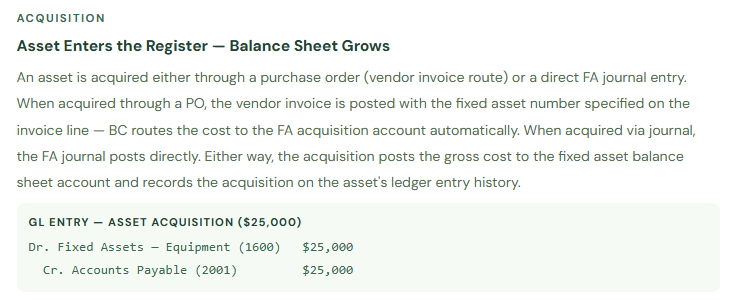

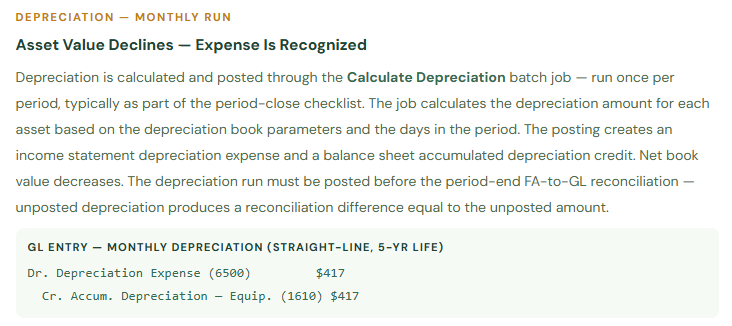

The FA Lifecycle — Acquisition Through Disposal

Every fixed asset in BC goes through a lifecycle that generates specific GL entries at each stage. Understanding what each stage does to the balance sheet and income statement prevents the most common FA-to-GL reconciliation problems.

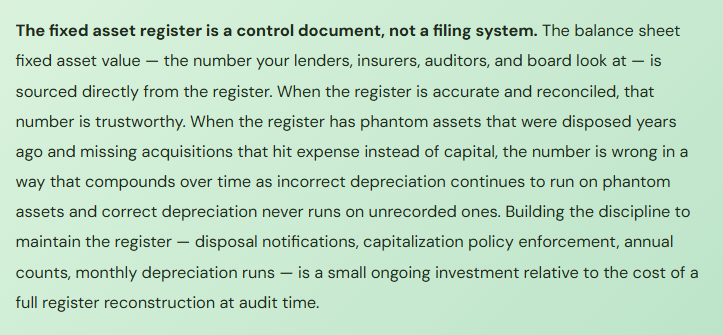

The FA-to-GL Reconciliation

The period-end fixed asset reconciliation confirms that the asset register and the general ledger are telling the same story. Run the Fixed Asset — Projected Value or Fixed Asset — Book Value report after each depreciation run. The total acquisition cost, total accumulated depreciation, and total net book value in the report should equal the balances of the corresponding GL accounts on the trial balance.

| Reconciliation Check | FA Report | GL Account | Common Difference Causes |

|---|---|---|---|

| Gross Asset Cost | Sum of all asset acquisition costs in FA register | Fixed Asset — [class] accounts | Asset acquired via PO but FA number not assigned; capitalized project cost posted to expense instead; asset added via GL journal without FA entry |

| Accumulated Depreciation | Sum of all depreciation posted in FA register | Accum. Depreciation — [class] accounts | Depreciation batch not run for the period; depreciation posted to wrong asset class; manual journal to accum. dep. GL account outside FA module |

| Net Book Value | Cost minus accumulated depreciation per FA register | Gross cost account minus accum. dep. account | Any of the above; also write-downs or reclassifications posted to GL without corresponding FA entry |

The FA Mistakes Finance Teams Discover at Year-End

⚠️ Assets Disposed but Still Depreciating in BC

When an asset is sold, scrapped, or traded in and the disposal isn’t recorded in BC, the asset continues to depreciate every month — reducing income statement depreciation expense correctly for something that no longer exists, leaving a net book value on the balance sheet for an asset no longer owned, and creating a phantom gross cost and accumulated depreciation that won’t tie to the physical count. This is the most common fixed asset register problem I encounter, and it almost always has the same cause: the disposal happened operationally (the equipment was removed) but nobody told Finance to post the disposal transaction in BC.

→ Create an internal process requiring a disposal notification to Finance any time a capital asset is removed from service, sold, traded in, or scrapped — regardless of the business reason. Define who in Operations is responsible for notifying Finance, and what information they need to provide (asset number, disposal date, disposal proceeds if any). Make disposal recording a named close checklist step: “Confirm no undocumented asset disposals with Operations” every period.

⚠️ Capital Expenditures Posted to Expense Instead of Fixed Assets

A vendor invoice for equipment arrives. AP processes it as a normal expense entry to a supplies or equipment expense account. The asset is in the building, operating, and depreciating economically — but it’s nowhere in the FA register and its cost hit the income statement in full in the period of purchase. The balance sheet is understated by the asset cost. The income statement is overstated by the same amount. The auditor notices the unusual equipment expense item and asks for documentation. This is a capitalization policy compliance failure, not an isolated bookkeeping error.

→ Define a capitalization threshold (typically $2,500–$5,000 depending on organization size) and document it as a written accounting policy. Train AP on identifying invoices that may represent capital expenditures — and train them that the correct routing for these invoices is a PO line with an FA number, not an expense journal line. Review the expense accounts for equipment, improvements, and technology monthly for any items that may need to be reclassified and capitalized.

⚠️ Depreciation Run Not Part of the Period-Close Checklist

The depreciation run in BC doesn’t happen automatically. Someone has to run the Calculate Depreciation batch job and post the results. In organizations where the FA module was set up during implementation and then handed off to a Finance team that wasn’t part of the implementation, this step is frequently missing from the close checklist — because it wasn’t explicitly added to the documentation. The result is a period that closes without depreciation, followed eventually by a large catch-up depreciation posting that makes the income statement look unusual and requires explanation.

→ Add “Run and post Calculate Depreciation batch job for all depreciation books” explicitly to the period-close checklist — not as an implied step under “post adjusting entries” but as a named, assigned task with a specific sequence dependency. It should run after all acquisitions for the period are posted (so new assets are included) and before the period-end FA-to-GL reconciliation (so the reconciliation reflects the current depreciation balance).

⚠️ No Physical Asset Count — Register and Reality Drift Silently

The FA register is a system record. Physical assets are real objects. They diverge silently over time: equipment gets scrapped without a disposal entry, assets are transferred between locations without a reclassification entry, serial numbers in the register don’t match the actual units on the floor. Organizations that never reconcile the register to physical reality typically discover the divergence at a year-end audit when the auditors request the physical count supporting the balance sheet — and it doesn’t exist. Reconstructing it from vendor invoices and disposal records going back years is an unpleasant project.

→ Conduct a physical fixed asset count at least annually — ideally before year-end close so that any disposals or additions identified can be posted before the financial statements are finalized. Match every item on the physical count to an asset card in BC. Every card in BC that can’t be matched to a physical item needs a disposal or write-off transaction. Every physical item that can’t be matched to a card needs an addition. The register should reflect reality.

Quick Reference: Do’s and Don’ts

✓ Do This

- Define FA Class and Subclass structure aligned with your balance sheet before creating any asset cards

- Review FA Posting Group GL account assignments before posting any acquisitions

- Document depreciation method, useful life, and salvage value by asset class as a written accounting policy

- Include Calculate Depreciation as an explicitly named step in the period-close checklist

- Post the depreciation run before the FA-to-GL reconciliation step in the close

- Create an internal disposal notification process from Operations to Finance

- Define and document your capitalization threshold — train AP on applying it

- Conduct a physical fixed asset count annually and reconcile to the BC register

- Reconcile FA register (cost, accum. dep., NBV) to GL accounts at every period close

- Use the non-integrated tax book for MACRS/IRS depreciation — keep it separate from the GAAP GL book

✗ Don’t Do This

- Post asset acquisitions via general journal to the fixed asset GL account without creating an FA card and using the FA journal

- Skip the depreciation run and expect it to catch up automatically in a future period

- Allow disposed assets to continue depreciating in BC because “nobody told Finance”

- Post capital expenditure invoices to expense accounts because it was faster than routing through an FA number

- Use a single FA Posting Group for all asset types — different classes need separate GL account routing

- Assume the FA register is accurate without an annual physical count to verify it

- Use manual depreciation as the default method for convenience — it removes the automation benefit

- Post disposal proceeds as a simple revenue journal without using the FA disposal transaction type — it leaves the asset on the register

- Ignore the FA-to-GL reconciliation at period close because “fixed assets rarely change”

Up Next:

Fixed assets are in good shape. Next, we’re moving to a topic that affects every organization that does business across currency boundaries: Budgeting and Forecasting in Business Central — the native BC budget tool, how to enter budgets by account and dimension, how to use budget vs. actual reporting in Financial Reports, what BC does well for budgeting, what it doesn’t do well, and the practical guidance on when to use BC’s budget feature and when to keep your planning process in a dedicated tool. If you’ve ever wanted the budget variance column in your monthly management report to actually mean something, this post explains what it takes to get there.

Until then — run your depreciation every period, post your disposals the same week they happen, and schedule an asset count before year-end.

— Bobbi

D365 Functional Architect · Recovering Controller

Leave a Reply