Asset books, depreciation methods, acquisition and disposal accounting, mid-year conventions, and the configuration decisions that determine whether your fixed asset register and your general ledger agree at year end — and why they so often don’t.

Why Fixed Assets Is More Complex Than It Looks

On the surface, fixed assets seems like a straightforward module: you acquire an asset, you depreciate it over its useful life, and eventually you dispose of it. Three steps, clean lifecycle, done.

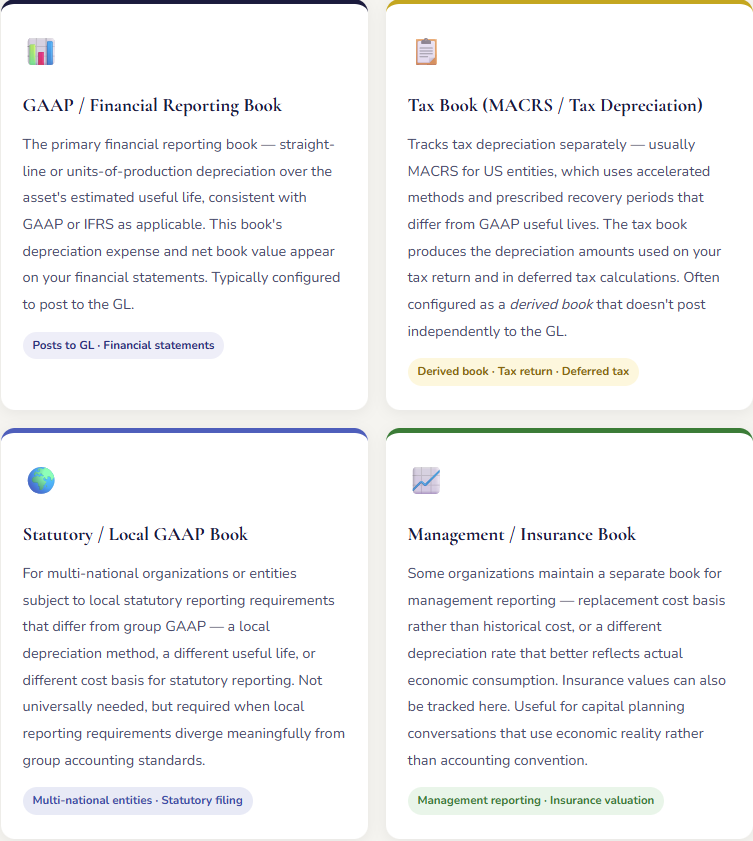

In practice, the complexity comes from a few places. First, most organizations need to track assets differently for different purposes simultaneously — GAAP book depreciation for financial reporting, MACRS accelerated depreciation for tax returns, and sometimes a third set of records for statutory or management reporting. D365 F&O handles this through the concept of multiple value models (called books in current terminology) attached to each asset, each with independent depreciation schedules. Understanding how books work is the foundational concept that makes everything else in this module make sense.

Second, the depreciation calculation in F&O depends on several interacting configuration choices — the depreciation method, the useful life, the convention (when in the year does depreciation start?), and the salvage value — and small differences in any of these produce materially different expense amounts over the life of the asset. Those choices need to be made intentionally, documented, and consistent with your accounting policies.

Third, fixed assets spans the line between Finance and Operations in a way that creates accountability gaps. Finance configures and manages the books. Operations — facilities, IT, production — physically uses, moves, modifies, and disposes of assets. When Operations doesn’t communicate changes to Finance, the register drifts from reality. This is the origin of every “we can’t find it” situation I described above.

Value Models (Books) — The Architecture That Makes Multiple Reporting Purposes Work

The most important design concept in D365 F&O Fixed Assets is this: a single physical asset can have multiple value models — also called books — attached to it, each running its own independent depreciation calculation, posting to its own set of GL accounts, and producing its own net book value. The asset is one thing. The books are multiple views of that asset for different accounting purposes.

Each book attached to an asset has its own service life, its own depreciation method, its own convention setting, and its own posting profile — which means depreciation from the GAAP book posts to your depreciation expense account on the income statement, while the tax book either posts nowhere (if it’s a derived non-posting book) or posts to a separate set of tax-basis accounts. You get one physical asset register with multiple simultaneous accounting views. This is the feature that makes the Fixed Assets module genuinely powerful for organizations with multiple reporting obligations.

Depreciation Methods — Choosing the Right One and Understanding the Difference

D365 F&O supports a wide range of depreciation methods. Most organizations need two or three. Here are the ones that matter most and what they produce.

01 Straight-Line Life Remaining

Most Common — GAAP

Divides the remaining depreciable cost evenly over the remaining useful life. Produces equal depreciation expense in every period after acquisition (adjusted for partial-year conventions). The most common GAAP depreciation method for most asset classes.

$100,000 asset, 10yr life, $0 salvage

Annual depr: $10,000 / yr — every year

02 Reducing Balance / Declining Balance

Accelerated — Tax / Bonus

Applies a fixed percentage to the net book value each period — front-loads depreciation expense into the early years of the asset’s life. Common for tax purposes (and the basis of MACRS). The percentage is typically 150% or 200% of the straight-line rate, switching to straight-line when that produces higher expense.

$100,000 asset, 200% DB, 10yr life

Yr 1: $20,000 · Yr 2: $16,000 · Yr 3: $12,800

03 Units of Production

Activity-Based

Depreciation is calculated based on actual usage — machine hours, units produced, miles driven — rather than time elapsed. Expense is highest in periods of high activity and low in periods of low activity. Matches expense recognition to asset consumption, which is conceptually cleaner for production equipment with variable utilization.

$100,000 asset, 1M unit life

Yr 1 (120K units): $12,000

Yr 2 (80K units): $8,000

04 Sum-of-the-Years’ Digits

Sum of Years

Another accelerated method — applies a declining fraction based on the sum of the asset’s years of useful life. Less common than declining balance but produces a similar front-loaded pattern. Occasionally seen in legacy systems being migrated to F&O; less often the method of choice for new implementations.

10yr life, sum = 55 (10+9+8…+1)

Yr 1 fraction: 10/55 = 18.2%

Yr 2 fraction: 9/55 = 16.4%

05 MACRS (US Tax Depreciation)

US Tax

Modified Accelerated Cost Recovery System — the standard US tax depreciation framework. F&O implements MACRS tables directly, including the half-year, mid-quarter, and mid-month conventions. The recovery period is determined by asset class (5-year for computers and autos, 7-year for most equipment, 39-year for commercial real estate). Configure the MACRS method and recovery period; F&O applies the correct rates automatically.

5-yr MACRS, half-year convention

Yr 1: 20.0% · Yr 2: 32.0%

Yr 3: 19.2% · Yr 4: 11.5%

06 Manual Depreciation

Manual / Irregular

For assets with irregular depreciation schedules — assets acquired in special lease structures, assets subject to impairment adjustments, or assets where the depreciation amount is determined externally and entered manually each period. The system doesn’t calculate; you enter the amount. Requires discipline to keep current; not appropriate where a formula-based method applies.

- Amount entered by user each period

- No automatic calculation

- Requires periodic manual input

Depreciation Conventions — The Detail That Changes Your First-Year Number

A depreciation convention determines how much depreciation is recorded in the year an asset is acquired and in the year it’s disposed of. This sounds like a technical detail. It produces material differences in Year 1 depreciation expense that directly affect your income statement, and it needs to match your accounting policy.

| Convention | What It Does | Common Use | Year 1 Impact on $100K / 10yr Asset |

|---|---|---|---|

| None (Full Year) | Full year’s depreciation in the year of acquisition, regardless of when during the year the asset was purchased. | Conservative GAAP approach; maximizes first-year expense | $10,000 — even if acquired December 31 |

| Half Year | Half a year’s depreciation in the year of acquisition and half a year’s in the year of disposal, regardless of actual acquisition date. | Most common GAAP convention; also the default MACRS convention for most asset classes | $5,000 — regardless of whether acquired January or November |

| Full Month | A full month’s depreciation in the month of acquisition. If acquired mid-month, you still get the full month. | Common for leasehold improvements and real property where monthly precision matters | $833/mo × months remaining in year |

| Mid Month | Treats acquisition as occurring on the 15th of the acquisition month — splits the first and last month. | Required for residential and commercial real property under MACRS (mid-month convention) | Half of the month’s depreciation for acquisition month |

| Mid Quarter | Treats acquisition as occurring at the midpoint of the quarter in which the asset was purchased. | Required under MACRS when more than 40% of depreciable assets are placed in service in Q4 | Variable — depends on which quarter the asset was acquired |

| Actual Days | Calculates depreciation based on the exact number of days the asset was in service during the year. | Used when precise day-level proration is required — less common for most asset classes | $10,000 × (days in service / 365) |

🎓 Why Convention Matters More Than You’d Think

Here’s a scenario that illustrates the stakes: your organization acquires $2 million of manufacturing equipment in Q4. Under the half-year convention — the default for most organizations — you record $100,000 of depreciation on that equipment in the current year (assuming a 10-year straight-line life). Under the “full year” convention, you record $200,000. Under actual days, if it was acquired December 15, you record about $4,500.

On a $2 million acquisition, the difference between the half-year convention and the full-year convention is $100,000 of depreciation expense. That’s a material income statement difference driven entirely by which convention box you selected in setup. This is not a place for “let’s use the default and revisit it later.” Get the depreciation convention right before the first asset is acquired.

The Fixed Asset Lifecycle in F&O — From Acquisition to Disposal

Every Asset Goes Through the Same Arc — Here’s What F&O Does at Each Stage

- Acquisition — Creating the Asset Record and Recording Cost

- An asset can enter F&O in several ways: posted from a purchase order (the cleanest path, where the PO receipt creates the asset automatically), posted from a free text invoice, posted from a fixed asset journal, or migrated as an opening balance during implementation. Each path results in an asset record with a book cost established on the acquisition date. That cost is the depreciable base — get it right from the start, because correcting it later requires an adjustment transaction that creates an audit question.

- Capitalization vs. Expense — The Policy Decision That Happens Before Posting

- Not every expenditure on a long-lived item is a capital acquisition. Routine maintenance is expensed. Major improvements that extend useful life are capitalized. The threshold — below which everything is expensed, above which capitalization is evaluated — is your organization’s capitalization policy. That policy needs to be documented and communicated to the people entering transactions, because F&O won’t prevent you from capitalizing a $150 printer cartridge or expensing a $50,000 equipment overhaul. The policy is the control; the system is the record.

- Depreciation Proposal and Posting

- Depreciation in F&O is not automatic — it runs when you execute the Depreciation Proposal process, which calculates the depreciation amounts for the period for all assets in all books, creates a journal with those amounts, and waits for you to review and post it. Most organizations run this monthly as part of their period-close process. The proposal can be reviewed before posting — confirm the totals look reasonable, investigate any asset that shows an unexpected amount, then post the journal. Depreciation expense hits the income statement only after the journal posts.

- Adjustments — Cost Adjustments, Revaluations, Impairments

- After acquisition, assets can be adjusted for additional costs (a subsequent capital improvement), write-downs (impairment under GAAP or IFRS), or revaluations (common under IFRS). Each type of adjustment has a specific transaction type in F&O that produces the correct GL entries and updates the asset’s depreciable base accordingly. Using the wrong transaction type — entering an impairment as a cost adjustment, for example — produces incorrect financial results that are difficult to untangle after the fact.

- Transfer — Moving an Asset Between Locations, Departments, or Entities

- When a fixed asset moves between locations, departments, cost centers, or legal entities, the transfer should be recorded in F&O — not as a disposal and re-acquisition, but as a transfer transaction. For intra-entity transfers, this updates the financial dimensions on the asset record so future depreciation posts to the correct cost center. For inter-entity transfers, the transaction is more complex and involves both the selling and receiving legal entities. Undocumented physical asset moves are how the fixed asset register drifts from reality.

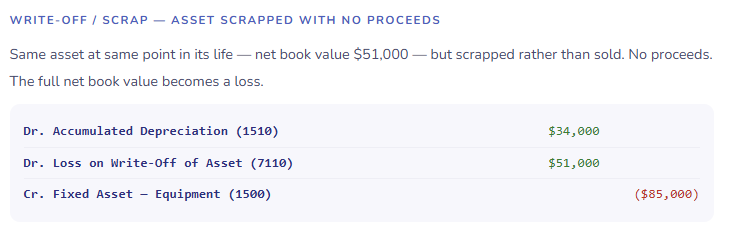

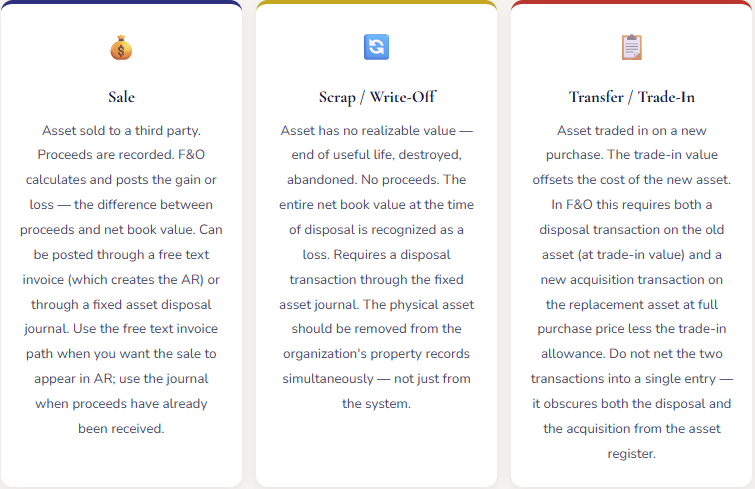

- Disposal — Sale, Scrap, or Write-Off

- When an asset leaves the organization — sold, scrapped, abandoned, destroyed, traded in — the disposal must be recorded in F&O through a disposal transaction that removes the gross asset cost and accumulated depreciation from the balance sheet, records any proceeds received, and posts the resulting gain or loss to the income statement. Failing to record a disposal leaves a fully depreciated ghost asset on the books — it doesn’t affect current depreciation expense (there’s nothing left to depreciate), but it overstates gross asset cost and accumulated depreciation indefinitely and creates confusion during physical counts and audit procedures.

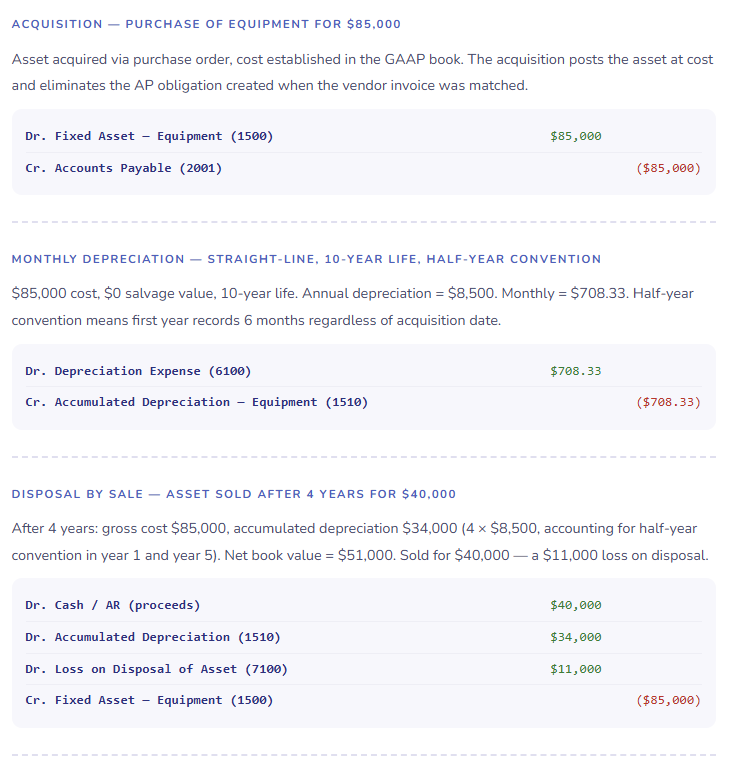

What Fixed Asset Transactions Look Like on the GL

Four Key Fixed Asset Transaction Types — The GL Entries Behind Each One

Disposal Paths in F&O — Three Scenarios, Three Different Transactions

The Fixed Asset Register — Keeping It Current

The fixed asset register is only as accurate as the processes that maintain it. Configuration gets you a well-structured register on day one. Operational discipline keeps it accurate in year three. Here’s the framework that works.

| Event | Required F&O Action | Who Needs to Tell Finance |

|---|---|---|

| New asset purchased | Acquisition transaction posted; asset record created with correct book, useful life, convention, and financial dimensions | Accounts Payable (from PO path) or whoever initiates the purchase |

| Asset moved to a different location or department | Transfer transaction posted; financial dimensions updated so depreciation charges the correct cost center going forward | Facilities / IT / Operations — whoever physically moved it |

| Capital improvement to existing asset | Adjustment transaction posted to increase the asset’s cost basis; revised useful life if the improvement extends service life | Whoever authorized and procured the improvement |

| Asset sold | Disposal transaction posted with proceeds; gain or loss calculated and posted to income statement | Whoever negotiated the sale — usually Operations or Management |

| Asset scrapped or destroyed | Write-off transaction posted; loss recognized; asset removed from register | Facilities, Operations, or whoever discovered/authorized the scrapping |

| Asset temporarily idle | Update the asset status in F&O; confirm whether depreciation should continue or be suspended per accounting policy | Operations — who knows the asset is idle |

| Annual physical count discrepancy | Investigate each discrepancy; post appropriate disposal or acquisition transactions based on findings; never adjust without investigation | Finance owns the investigation; Operations provides physical access and information |

The column that matters most in that table is the last one. Every row in the register depends on someone outside Finance communicating a change. The communication channel doesn’t have to be elaborate — a monthly email, a quick internal request form, a flagged field in your facilities management system — but it has to exist and be used consistently. Without it, Finance is the last to know about changes to assets that have been on the books for years.

The Mistakes That Create the Audit Findings

⚠️ Wrong Depreciation Convention — Discovered at Year-End After Twelve Months of Wrong Expense

This is the mistake that’s hardest to catch and most expensive to correct. An organization acquires $3 million of equipment in a single fiscal year and configures the depreciation convention incorrectly — say, “Full Year” when the policy requires “Half Year.” Twelve months of monthly depreciation proposals run without anyone noticing. At year end, the external auditors question the depreciation rate on the new equipment. The investigation reveals the convention has been wrong from day one. Twelve months of expense need to be reversed and recalculated. The current year’s financials are restated. This is not a hypothetical — it is among the more common fixed asset audit findings at organizations implementing a new ERP.

→ Review and document your depreciation convention choices before the first depreciation proposal is posted in production. Have your Controller or external auditors confirm that the convention configured in each value model matches your stated accounting policy. Run the first depreciation proposal in a test environment and compare the calculated amounts to what you’d expect given the convention — a sanity check takes twenty minutes and prevents a year-end restatement conversation.

⚠️ Disposed Assets Left on the Register — Ghost Assets at Every Physical Count

The ghost asset problem is endemic across organizations that haven’t established a communication process between Operations and Finance for disposals. Equipment is surplused, traded in, scrapped, or stolen. Operations handles the physical disposition. Finance never hears about it. The asset sits on the books — fully depreciated, probably, but still inflating gross asset cost and accumulated depreciation. Year after year, the gap between the physical asset base and the register grows. When the external auditors or the insurance company requests a physical count and reconciliation to the register, the cleanup effort is significant. At one organization I worked with, the cleanup identified $1.4 million of gross asset cost that needed to be written off in a single period.

→ Establish a formal asset disposal notification process — a simple form, an email alias, a workflow in your facilities management system — that routes disposal information to Finance for every asset with a cost above your capitalization threshold. Make it part of the onboarding for facilities, IT, and operations managers. Include a question about pending disposals in your quarterly close conversations with those teams. Conduct an annual physical count and reconcile findings to the register before closing the fiscal year.

⚠️ Maintenance Expense Capitalized — Revenue vs. Capital Not Clearly Defined

Without a documented and communicated capitalization policy, the line between expensing and capitalizing is drawn differently by every person who posts a transaction. A $12,000 HVAC repair gets capitalized because it “seems big.” A $35,000 roof replacement gets expensed because “it’s maintenance.” Neither decision is informed by a consistent policy — they’re informed by whoever processed the invoice that day. The result is an income statement where depreciation expense and repair expense are both unreliable, and a balance sheet where fixed assets don’t represent the actual capitalized asset base.

→ Document your capitalization policy — the dollar threshold, the betterment versus maintenance distinction, the treatment of installation and freight costs, and the useful life guidelines by asset class — before go-live. Communicate it to AP, Procurement, and the managers who approve capital expenditures. Review it annually. F&O can enforce a required fixed asset association on GL accounts designated for capital expenditures, which helps — but the policy has to exist before the system can support it.

⚠️ Depreciation Proposal Not Run — Or Run But Not Posted — For Multiple Periods

Depreciation in F&O is not automatic. Someone has to run the Depreciation Proposal and then post the resulting journal. When this step is missed — in a busy close, during a staff transition, when the person responsible is on leave and no backup was trained — depreciation expense is understated for that period. If it’s caught in the same period, it’s a posting oversight. If it’s caught after the period closes, it requires a prior-period adjustment. If it’s caught at year end after multiple periods were missed, the cumulative adjustment is material, the financial statements for the missed periods are wrong, and the conversation with auditors is uncomfortable.

→ Add “Run and post depreciation proposal” to your month-end close checklist as a required, owned step with a specific person responsible and a designated backup. In the checklist, include the expected depreciation amount range — if the posted amount differs from the prior month by more than a defined threshold without a new acquisition or disposal explaining the difference, investigate before considering the step complete. The backup person should run the proposal in test at least twice a year so the step isn’t foreign to them when they need to cover it.

⚠️ Fixed Asset GL Accounts Not Reconciled to the Asset Register

The fixed asset subledger — the register of individual assets with their costs, accumulated depreciation, and net book values — should roll up to agree exactly with the fixed asset GL accounts on your balance sheet. If someone has posted a manual journal entry to a fixed asset GL account, or if an asset was posted through the wrong transaction type, or if there’s an opening balance migration error that was never caught, the subledger and the GL will disagree. The disagreement is usually invisible until you run the reconciliation report — which many organizations run once a year at audit time and discover a difference they have to trace back through months of transactions to explain.

→ Run the fixed asset to GL reconciliation report monthly, not annually. It should run to zero difference. If it doesn’t, investigate and resolve the discrepancy in the same period it’s identified. Treat an unreconciled fixed asset balance the same way you treat an unreconciled bank balance — a month-end close requirement with a completion standard, not an annual cleanup exercise.

Quick Reference: Do’s and Don’ts

✓ Do This

- Document your depreciation convention for each asset class before the first transaction posts — and have your Controller confirm it matches accounting policy

- Configure multiple value models where needed: GAAP book posting to GL, derived tax book for MACRS

- Establish and communicate a written capitalization policy before go-live

- Add “Run and post depreciation proposal” to the period-close checklist with a named owner and backup

- Sanity-check the first depreciation proposal output against manual calculations before posting

- Establish a formal asset disposal notification process involving Operations, Facilities, and IT

- Record asset transfers between locations and departments — don’t leave dimension coding unchanged when assets move

- Run the fixed asset to GL reconciliation monthly, not annually

- Conduct an annual physical count and reconcile to the register before closing the fiscal year

- Investigate every physical count discrepancy — don’t net them or write off without tracing the cause

- Record trade-ins as separate disposal and acquisition transactions — do not net

- Use the correct disposal type for each situation: sale, scrap, or write-off produce different GL entries

✗ Don’t Do This

- Accept the default depreciation convention without confirming it matches your accounting policy

- Use a single value model when your organization has GAAP and tax reporting obligations

- Allow depreciation proposals to go unrun for multiple periods without a period-close control catching it

- Leave disposed assets on the register because nobody told Finance they were gone

- Post manual journal entries directly to fixed asset GL accounts — all adjustments go through the Fixed Assets module

- Capitalize maintenance expenses or expense capital improvements without a documented policy guiding the decision

- Run the fixed asset to GL reconciliation only at audit time

- Post asset improvements as new asset acquisitions — they belong as adjustments to the existing asset record

- Use a write-off transaction for an asset that was sold — it eliminates proceeds and misstates the gain/loss

- Net a trade-in against a new acquisition — record both transactions separately

- Skip the physical count because “the system should know where everything is” — it knows what was entered, not what’s actually there

- Allow useful life or residual value to go unchanged when an impairment or major improvement changes those estimates

The closing thought from the controller who found the storm-damaged equipment on the books: the fixed asset register is a living document. It describes what your organization owns, where it is, how much it cost, how much has been charged to expense, and what it’s currently worth on the books. When it’s accurate, it’s one of the most useful documents in your financial records — it supports insurance discussions, capital budgeting decisions, audit procedures, and management’s understanding of asset condition and replacement timing. When it’s inaccurate, it’s a source of confusion that compounds with every year that passes without a reconciliation.

D365 F&O gives you the tools to keep it accurate — multiple books for different reporting purposes, a full transaction audit trail, automatic depreciation calculation, and reconciliation reporting that flags discrepancies before they accumulate. The tools are there. Using them requires a few solid habits and a communication process between Finance and the people who physically work with your assets every day. Those habits and that communication process are worth building from day one of go-live. The alternative is a register that describes an organization that hasn’t quite existed for several years, discovered at the worst possible moment by your auditors.

Up Next:

We’ve worked through the full financial foundation of D365 F&O — from the chart of accounts through procurement, inventory, collections, treasury, and now fixed assets. It’s time to talk about the reporting layer that sits on top of all of it: Financial Reporting in D365 F&O — Management Reporter (now Financial Reporter), how to build financial statements that actually serve your leadership, dimension-based reporting, and the difference between having accurate data in your system and having reporting infrastructure that turns that data into decisions. If you’ve ever exported a trial balance to Excel and built a financial statement by hand, this post will show you what you were missing.

Until then — run your depreciation proposal, reconcile your asset register to the GL, and please ask Operations whether anything has been scrapped or sold recently without a disposal transaction.

— Bobbi

D365 Functional Architect · Recovering Controller

Leave a Reply