Bill of materials, routing, production order costing, WIP accounting, standard cost variance analysis, and the Finance-owned configuration decisions that determine whether manufactured goods inventory is accurately valued and variance accounts tell a useful story.

The Finance Scope in Manufacturing: What You Own Before Production Starts

D365 F&O’s manufacturing module involves configuration owned by multiple functions — Engineering owns the bill of materials, Operations owns routing and work center setup, Production Planning owns scheduling. But before any production order can post a financially meaningful entry, Finance must own four configuration decisions that determine the entire cost accounting foundation for manufactured goods.

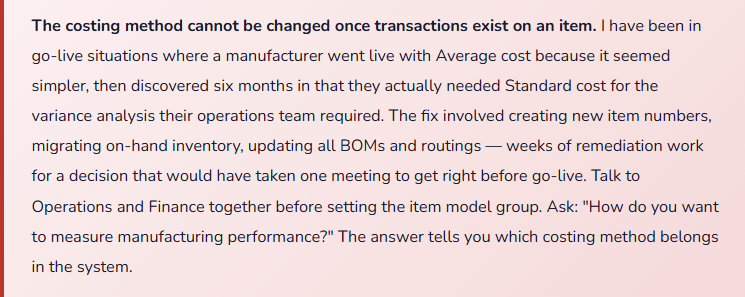

First: the costing method. Set on the item model group — cannot be changed after transactions exist for an item. Standard, Average, FIFO, or Specific. The costing method determines how cost flows through production and what “variance” even means. This is not a default to accept; it is an accounting policy election.

Second: the standard cost version. For standard costing (the method used by the large majority of discrete manufacturers in D365), the standard cost version holds the expected cost per manufactured item — the denominator against which actual production costs are compared to produce variances. The standard cost must be calculated, reviewed, approved, and activated by Finance before the production year begins.

Third: the production posting profile. The GL accounts that receive WIP postings, finished goods output, and production variances are all Finance-owned configuration. Each variance type maps to an account. If five variance types all map to a single “Production Variance” account, the financial statement will show the total but analysis will require production detail reports to decompose it. If each variance type maps to its own account, the trial balance itself tells the story.

Fourth: work center cost rates. Each work center carries labor and overhead rates used to absorb production costs into manufactured goods. These rates are the mechanism by which labor expense and overhead are transferred from P&L accounts into inventory value on the balance sheet. Rates that are stale or never set produce manufactured goods at material cost only — understating inventory, overstating expense, and distorting gross margin for every period the issue persists.

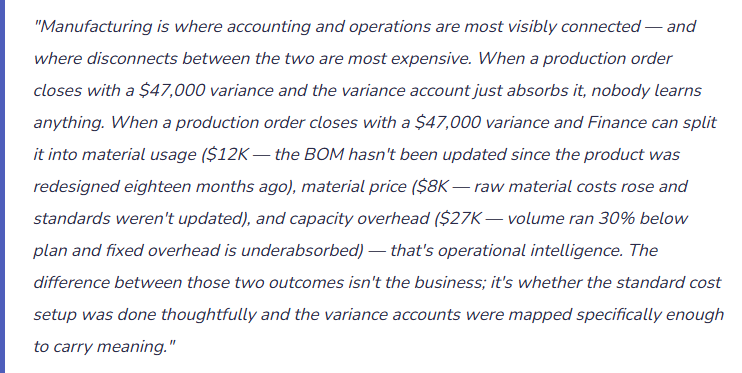

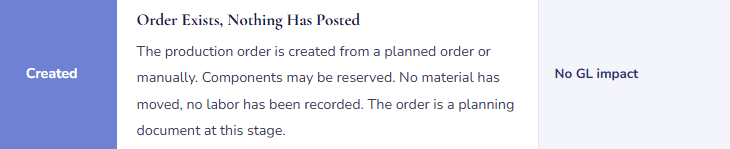

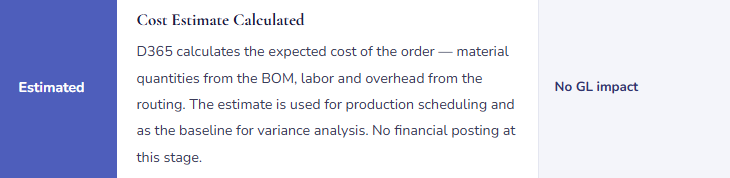

The Production Order Lifecycle — Five Statuses, Three GL Events

Not every production order status creates a GL posting. Finance needs to know which statuses matter financially, because that determines when WIP moves and when the balance sheet changes.

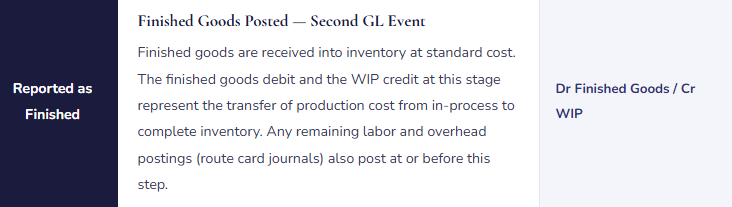

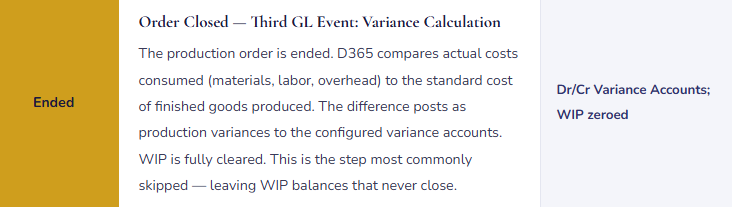

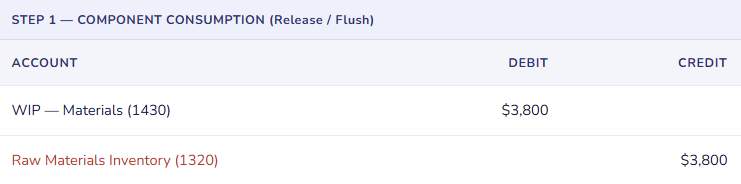

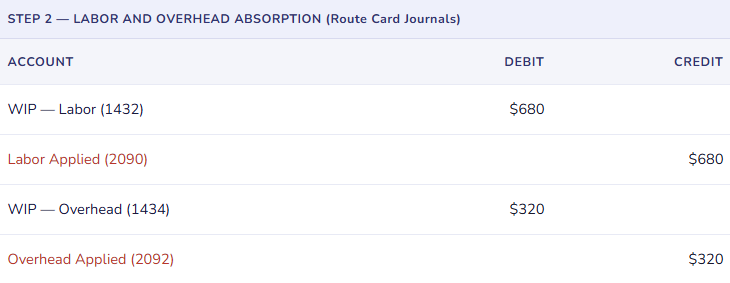

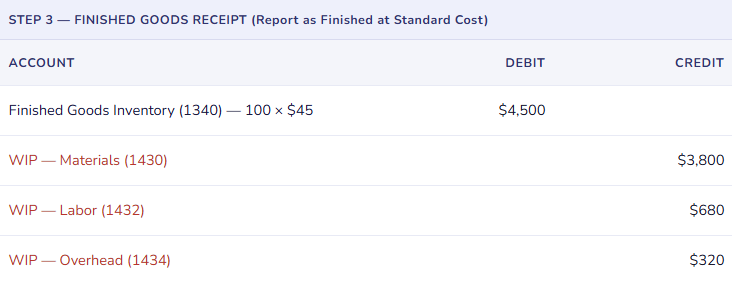

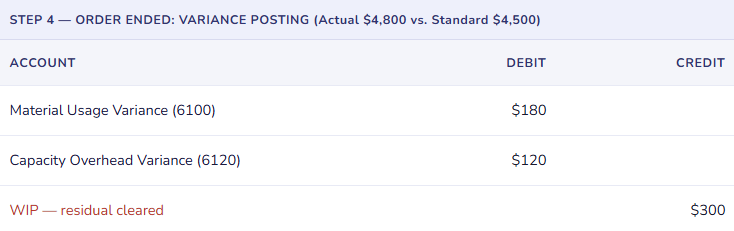

The Complete GL Flow for a Production Run

The variance entries in Step 4 are the financial output of the entire production cycle. The accounts they land in — and how specifically those accounts are defined — determine whether your income statement carries operationally useful information or a single undifferentiated “Production Variance” line that Operations ignores because Finance can’t explain it.

The Standard Cost Update — Finance’s Annual Manufacturing Obligation

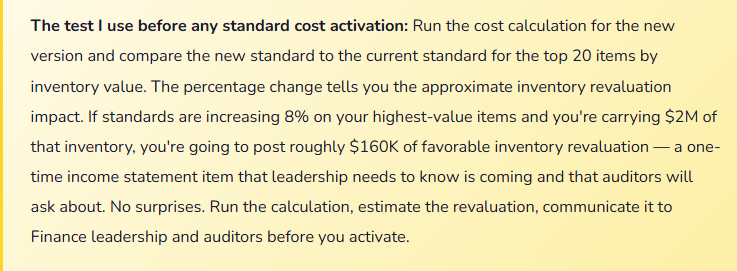

Standard costing requires that Finance maintain the standard cost version — the set of expected costs against which actuals are compared. That maintenance isn’t optional and it isn’t a one-time go-live activity. It is a recurring annual process, and for organizations with significant raw material price volatility or labor cost changes, it may need to occur more frequently.

The standard cost update process in D365 F&O: recalculate standard costs using updated component prices and routing rates, review the new standards against current market pricing, activate the new cost version, and accept the revaluation of on-hand inventory to the new standard. That last step — inventory revaluation — creates a GL posting that adjusts inventory value from the old standard to the new one. The revaluation entry flows through the inventory revaluation account defined in the posting profile. Finance must anticipate and explain that posting at the time of the annual standard cost update; it is not a variance, it is a policy-required restatement of inventory to current standard.

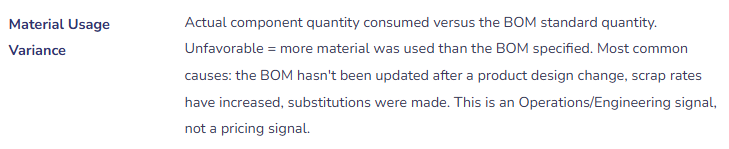

Production Variance Types — What Each One Tells You

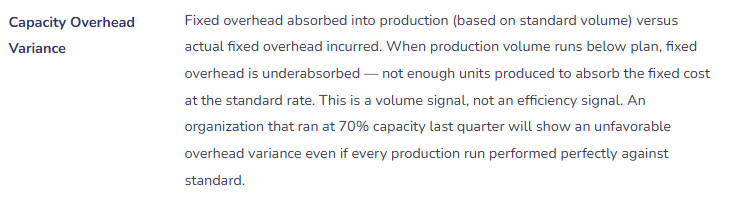

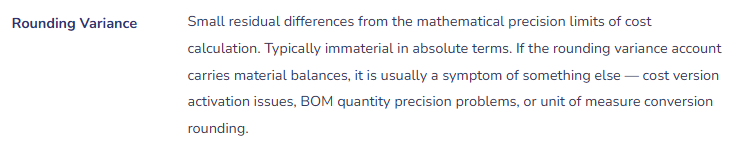

D365 F&O decomposes production order variances into specific types that can be mapped to distinct GL accounts. Here is what each variance type means operationally and why Finance should care about it separately.

Costing Methods — The Decision You Cannot Easily Undo

📌 Standard Cost

- Inventory valued at a predetermined standard. Actual cost differences post as variances. Predictable COGS, meaningful variance analysis, requires annual standard update discipline. The dominant choice for discrete manufacturers with stable production processes.

- Best for: discrete manufacturing with repeatable processes and meaningful budget/standard

⚖️ Weighted Average

- Inventory valued at a running weighted average recalculated after each receipt. Smooths price volatility. No variance accounts — cost adjustments flow through inventory value. Harder to reconcile to specific purchase invoices. No standard update process required.

- Best for: process industries, commodity-driven businesses where price volatility is the dominant factor

🔢 FIFO

- Oldest cost layers consumed first. In rising cost environments, FIFO produces lower COGS and higher inventory value than average. Cost layer complexity increases with transaction volume. The inventory closing process settles cost layers — must run monthly.

- Best for: businesses where FIFO matches physical flow and lower COGS presentation serves reporting objectives

🏷️ Specific (Lot/Serial)

- Each individual item tracked at its own cost. Highest precision. Requires lot or serial number tracking for every unit. Administrative overhead is substantial. Appropriate for high-value, unique items where individual cost attribution is required for margin analysis or regulatory traceability.

- Best for: aerospace, defense, high-value capital equipment, items with regulatory traceability requirements

Five Mistakes That Make Manufacturing Finance Difficult to Close

⚠️ Work Center Cost Rates Left at Zero — Overhead Never Absorbed Into Inventory

- At go-live, work centers were created and production routing was configured but nobody set the labor rates and overhead rates on the work centers. The setup looked complete — work centers had names, capacity definitions, calendar assignments. Production orders ran, route card journals posted. But because the rates were zero, the labor and overhead cost absorbed into WIP was zero. For twelve months, finished goods inventory carried only material cost. The income statement absorbed labor and overhead directly as period expense rather than flowing them through WIP into inventory cost. Gross margin was systematically understated because manufactured goods were valued at materials only. The auditor found it at year-end.

- Fix: Work center cost rates are a Finance responsibility, not an Operations responsibility. Before any production order goes live, Finance must confirm that every work center in every routing used for production has labor rates and overhead rates populated and that a standard cost calculation using those rates produces a reasonable per-unit cost. Run a test standard cost calculation against the production BOM before go-live, review the output by cost component (material / labor / overhead), and verify that the cost structure makes economic sense.

⚠️ Production Orders Not Ended — WIP Accumulates Indefinitely on the Balance Sheet

- The production team reports orders as finished and moves to the next order. Ending the order — the step that calculates variances and clears WIP — is treated as administrative cleanup rather than a required financial step. After six months, the WIP account carries balances from 200+ production orders that were physically complete but financially still open. The balance sheet shows $840,000 of WIP. The actual in-process orders represent maybe $120,000. The other $720,000 is finished — or scrapped, or never fully consumed — but the orders were never ended so WIP was never cleared. Period close takes an extra day because someone has to explain the WIP balance to the auditor.

- Fix: Production order ending is a Finance-required step, not an optional Operations cleanup task. Put a WIP aging report on the period-close checklist — any production order with a “Reported as Finished” status older than 48 hours that hasn’t been ended is an exception requiring investigation. Define a policy: all completed production orders must be ended within one business day of the finished goods receipt being confirmed. Assign accountability for that policy to Production Supervision with Finance enforcement at period close.

⚠️ All Variance Types Mapped to a Single Account — Variance Analysis Requires Going to Production Reports

- The production posting profile was configured with one “Production Variance” account receiving all variance types — material usage, material price, capacity usage, capacity overhead, rounding. The income statement shows a single production variance line. It could be $200K unfavorable because material prices rose, $200K unfavorable because volume was low and overhead underabsorbed, or $200K unfavorable because BOMs are stale and more material is being consumed than planned. Finance cannot tell from the trial balance which it is. Every variance explanation requires pulling production detail reports, sorting by variance type, exporting to Excel, and manually aggregating — a 45-minute exercise that could have been a 30-second trial balance review.

- Fix: Map each variance type to its own GL account in the production posting profile. Material Usage Variance, Material Price Variance, Capacity Usage Variance, Capacity Overhead Variance — each gets an account. The additional accounts cost nothing but a few rows in the chart of accounts. The analytical value is substantial: each month, the variance accounts in the trial balance tell Operations exactly where cost performance deviated from standard, without requiring Finance to build a report to explain it.

⚠️ BOMs Not Updated After Product Changes — Usage Variances Absorb Structural Differences

- Engineering redesigned a product eight months ago — changed a subcomponent, reduced the quantity of one material, added a new fastener. The change was implemented on the production floor. The BOM in D365 was not updated. Every production order since the redesign has generated a material usage variance — favorable for the reduced material, unfavorable for the new fastener, net unfavorable $3.20 per unit. With 4,000 units produced per month, $12,800 of monthly variance is flowing to the usage variance account. Finance investigates the usage variance quarterly, finds it attributable to the known design change, documents it as “known BOM discrepancy,” and moves on. The BOM never gets updated. The variance account carries a meaningful but entirely preventable balance every single month.

- Fix: Engineering change control must include a D365 BOM update as a required step — not a nice-to-have, not something that gets done “when there’s time.” The BOM is the financial cost recipe for the product. An outdated BOM produces predictable, persistent, explainable variances that Finance has to document every period. Establish a joint Engineering/Finance process for BOM updates: Engineering submits the change, Finance calculates the standard cost impact, the BOM is updated in D365 before the next production run using the changed design.

⚠️ Standard Costs Not Updated Annually — Standards Drift from Reality, Variances Lose Meaning

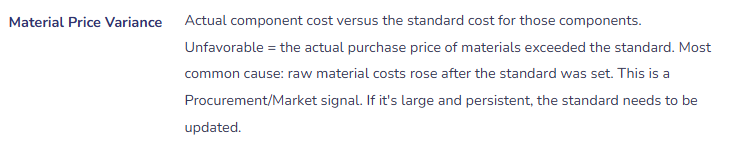

- Standards were set at go-live two years ago. Raw material costs have increased 18% since then. The standard hasn’t changed. Every production order generates an 18% material price variance — not because production performance is poor but because the standard no longer reflects the current cost of materials. The price variance account carries a large, persistent, unfavorable balance every month. Operations stopped paying attention to the variance report because “it just shows the material cost difference, not anything we can control.” The variance account that should be a performance management tool has become a catch-basin for structural cost drift that nobody feels responsible for fixing.

- Fix: Standard cost updates are an annual Finance obligation, not an optional system maintenance task. The process: recalculate standards using current component prices (pull the most recent purchase prices or vendor quotes), update work center rates to reflect current labor and overhead cost structure, activate the new cost version, revalue on-hand inventory, communicate the revaluation impact to Finance leadership. Document the effective date and the basis for the new standards. When standards are current, variance accounts measure performance. When they aren’t, variance accounts measure staleness — and nobody benefits from that.

Do This / Don’t Do This

✓ Do This

- Set costing method before go-live — it cannot be changed after transactions post

- Populate work center labor and overhead rates before any production order goes live

- Map each variance type to its own GL account in the production posting profile

- Include production order ending in the period-close checklist

- Run WIP aging report at every period close — flag orders open beyond 48 hours after completion

- Update standard costs annually and communicate the inventory revaluation impact in advance

- Require BOM updates as part of Engineering change control before next production run

- Run a test standard cost calculation before go-live to verify cost structure makes sense

- Review variance account balances monthly — persistent patterns signal a standards or BOM problem

✗ Don’t Do This

- Accept the costing method default without a deliberate Finance and Operations discussion

- Leave work center rates at zero — overhead will never reach inventory

- Map all variance types to one account — variance analysis will require manual reports forever

- Treat production order ending as optional cleanup — WIP accumulates and never clears

- Let BOMs drift from actual production — usage variances will be large, explainable, and preventable

- Let standard costs age beyond one year without review — variances stop measuring performance

- Skip the inventory revaluation communication when activating new standards — surprise income statement items damage credibility

Up Next:

Manufacturing covers how production cost flows through WIP to finished goods and variance. Next we tackle a configuration area that is almost universally underestimated at go-live: Tax Configuration in D365 F&O — the sales tax engine (tax groups, item tax groups, and the intersection model that determines the tax code), VAT setup for multi-country implementations, withholding tax, tax-exempt scenarios, and the tax calculation mistakes that produce financial statement misstatements that don’t surface until a tax audit.

Until then — set your costing method deliberately, populate your work center rates, map variance types to separate accounts, and end every production order within 48 hours of completion.

— Bobbi

D365 Functional Architect · Recovering Controller

Leave a Reply