Intrastat reporting for EU entities, import/export controls, country of origin and HS code tracking, dual-use item classification, landed cost calculation and duty accruals, free trade agreement eligibility, and the Finance setup that ensures trade compliance costs land in inventory cost rather than in a period-end surprise journal.

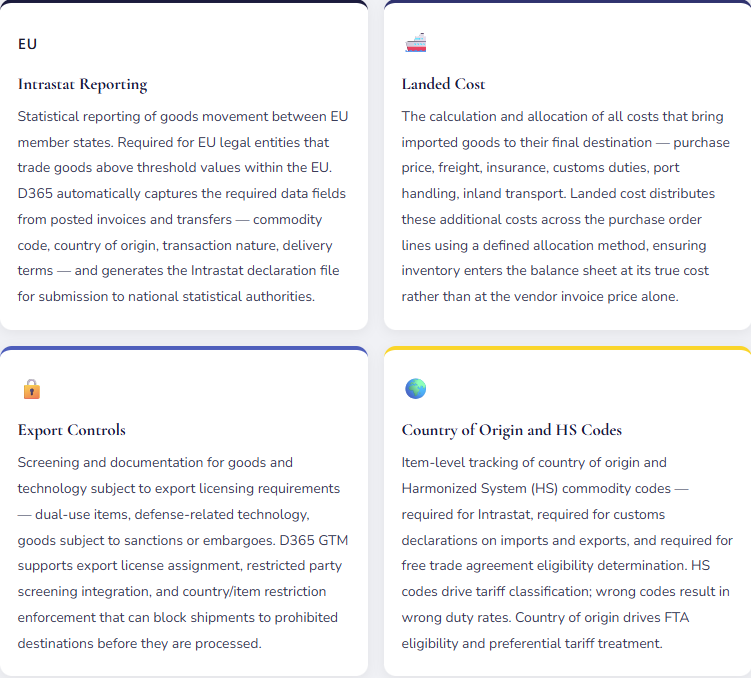

The Four Trade Compliance Areas D365 GTM Covers

Intrastat — What Finance Must Understand Before the First EU Transaction Posts

Intrastat is the EU’s system for collecting statistics on the movement of goods between member states. It is not a tax — it is a statistical declaration. But the penalties for late or incorrect filing range from administrative fines to mandatory corrections with audit trails, and in some member states, persistent non-compliance escalates to customs authority involvement. For Finance teams managing EU operations in D365 F&O, Intrastat is a monthly compliance obligation that the system can largely automate — if the item-level data is correct at the time transactions post.

Intrastat — Finance and Data Setup Requirements

- Commodity Codes (HS Codes) on Every Item

- Every item that will be reported in Intrastat must carry the correct commodity code — the 8-digit CN (Combined Nomenclature) code for EU trade. The commodity code drives the statistical classification that appears in the Intrastat declaration. A missing commodity code causes the item to fall out of the Intrastat transfer — it won’t appear in the declaration even if the transaction otherwise qualifies. An incorrect commodity code results in a filing that doesn’t accurately reflect the goods traded. Finance must work with the product or purchasing team to ensure commodity codes are populated on the item record before EU purchase orders or sales orders post.

- Country of Origin on Items and Procurement Records

- Country of origin is required on Intrastat declarations for dispatches (exports within the EU). It must be populated on the item record or on the purchase order if it varies by supplier. “Country of origin” for Intrastat purposes means the country where the goods were produced or substantially transformed — not necessarily where the vendor is located. A vendor in Germany supplying goods manufactured in China has a country of origin of China, not Germany. This distinction matters for Intrastat accuracy and for FTA eligibility assessment.

- Transaction Nature and Delivery Terms

- Intrastat declarations require transaction nature codes (sale, return, processing under contract, etc.) and delivery terms (Incoterms — EXW, FOB, CIF, DAP, etc.). These fields default from the transaction type and the shipping terms on the order — but Finance must confirm the defaults are correct. Incoterms drive whether freight and insurance are included in the statistical value reported; the wrong Incoterm produces an Intrastat statistical value that doesn’t match the commercial invoice value in ways that can trigger authority inquiries.

- Intrastat Threshold Monitoring

- Intrastat obligations apply when the value of intra-EU trade exceeds the national threshold — different for arrivals (imports from other EU states) and dispatches (exports to other EU states), and different by member state. D365 doesn’t automatically alert when a legal entity crosses the threshold; Finance must monitor the cumulative intra-EU trade value against national thresholds and initiate Intrastat registration before the first declaration period in which the threshold is exceeded. Filing before obligation is harmless; filing late carries penalties in most member states.

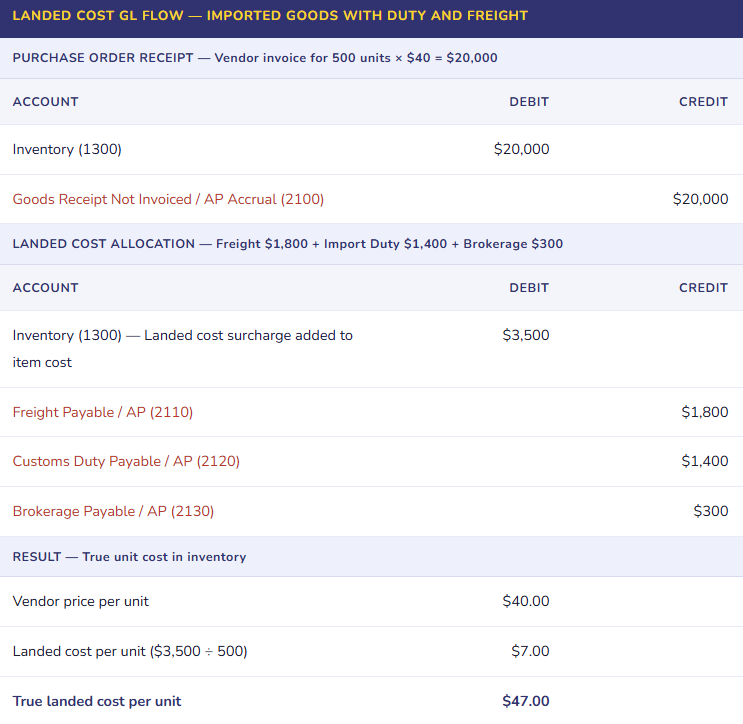

Landed Cost — Getting Inventory onto the Balance Sheet at Its True Cost

The vendor invoice price of imported goods is rarely the true cost of those goods to the business. Freight, insurance, customs duties, brokerage fees, port handling, and inland transport all add to the cost of getting the goods from the vendor’s facility to the warehouse. Landed cost is the sum of all those components — and it is what inventory should enter the balance sheet at, not just the vendor invoice price.

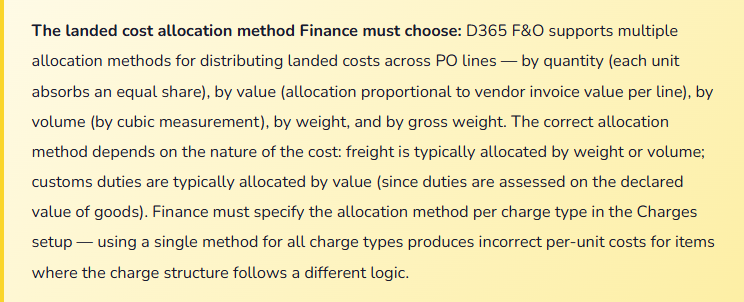

D365 F&O’s Landed Cost module (and the Charges functionality in standard procurement) provides mechanisms to allocate these additional costs across purchase order lines using defined methods. The Finance implication is direct: if landed costs are expensed as incurred rather than capitalized into inventory cost, the income statement absorbs freight and duty costs in the period they’re paid while the inventory balance carries the vendor price only. When the inventory sells, COGS is understated (the true cost wasn’t in it), gross margin is overstated, and every period-end inventory valuation understates the asset by the accumulated uncapitalized landed costs.

Export Controls — The Compliance Framework Finance Must Understand

Export controls in D365 F&O address the regulatory requirement to screen items, customers, and destinations against export license requirements, sanctions lists, and embargoes before a shipment is released. For Finance, the primary implications are two: the operational risk if a shipment is blocked mid-process (revenue disruption, customer relationship impact), and the liability risk if a controlled shipment proceeds without the required license (civil and criminal penalties).

| Export Control Element | What It Controls | Finance Implication |

|---|---|---|

| Dual-Use Item Classification | Items that have both civilian and military applications are classified as dual-use under EAR (US), EU Dual-Use Regulation, and equivalent national frameworks. Items with Export Control Classification Numbers (ECCNs) or EU dual-use codes require export licenses for specific destinations and end-users. | Revenue from dual-use item sales to controlled destinations cannot be recognized until the export license is in place — the sale is contingent on a regulatory approval. A sales order for a dual-use item that is booked and invoiced before license approval creates a contingent liability and may need revenue reversal if the license is denied. |

| Restricted Party Screening | Customer and end-user names screened against denied party lists (BIS Entity List, OFAC SDN list, EU consolidated list). D365 supports integration with third-party screening services for automated screening at order entry. | Shipments to sanctioned parties are prohibited regardless of the commercial terms. If a sale proceeds to a sanctioned party without screening, the resulting regulatory penalty can be a multiple of the transaction value. Revenue booked from a sanctioned-party transaction carries penalty exposure that may exceed the transaction amount. |

| Export License Assignment | For items and destinations requiring export licenses, the license must be assigned to the sales order in D365 before shipment. D365 tracks license utilization — remaining license value and quantity — against the licensed amount. | License tracking is a Finance compliance control. An export license authorizes a specific value of exports to a specific destination over a defined period. Exceeding license limits — either in value or quantity — constitutes a violation even if individual transactions appear compliant. Finance must monitor license utilization against the licensed ceiling. |

| Country/Region Restrictions | D365 GTM supports country/region restriction rules that block transactions with embargoed countries at the order entry level — preventing sales orders, purchase orders, or transfers to/from embargoed destinations from being created. | Embargo compliance is an absolute prohibition — there are no exceptions for commercial convenience. Blocking at order entry is the correct control point; Finance should confirm that country restriction rules are configured and active for all embargoed destinations before any international sales orders are entered in D365. |

Five Mistakes That Turn Trade Compliance into Finance’s Problem

⚠️ Commodity Codes Missing from Items — Intrastat Declarations Are Systematically Incomplete

An EU subsidiary goes live in D365 F&O. Intrastat is activated for the legal entity. The first month’s Intrastat transfer runs and Finance generates the declaration. The statistical authority rejects it: 34% of the line items reference a blank commodity code and cannot be reported. Finance investigates — the item master migration at go-live included item names, units, and cost groups, but commodity codes weren’t in scope because “that’s a logistics thing.” The items have been trading across EU borders for three months. Three monthly declarations need to be reconstructed manually, commodity codes need to be researched and assigned for all affected items (600+ items), and the corrected declarations require submission with an explanation of the delay. The statistical authority notes the systematic omission in the entity’s compliance record.

Fix: Commodity code population is a Finance and compliance responsibility at go-live — not a logistics afterthought. For any EU legal entity, the item master migration scope must include commodity codes for every item that will trade across EU borders. If the go-live item list doesn’t have commodity codes from the legacy system, a parallel workstream must assign them using the Customs Tariff and CN classification resources before the first intra-EU transaction posts. Build commodity code validation into the D365 item approval workflow — an item can’t be activated for purchasing or sales without a commodity code in EU legal entities. Catching the gap at item creation costs minutes; reconstructing three months of declarations costs days.

⚠️ Import Duties Expensed as Incurred Rather Than Capitalized into Inventory — COGS and Margin Are Both Wrong

A distributor imports goods from Asia. The import duties average 6.5% of the vendor invoice value. The accounting team processes customs duty invoices from the freight broker as a period expense — “Import Duties Expense” — in the period the goods clear customs. Inventory enters the balance sheet at the vendor invoice price only. When the goods sell, COGS reflects only the vendor cost. Gross margin appears to be 38%. The CFO benchmarks the business against industry peers showing 31–33% margins and concludes the business is exceptionally profitable. The actual margin, if duties were correctly capitalized into inventory cost, is 32.8% — within the industry range. Pricing decisions, sales compensation, and product line decisions have been made on the wrong margin for three years.

Fix: Customs duties, freight, and other import charges that are directly attributable to specific goods are inventory costs under both US GAAP (ASC 330) and IFRS (IAS 2). They must be capitalized into inventory cost — not expensed as incurred — for periods in which the related inventory is still on hand. D365 Landed Cost or the Charges functionality on purchase orders provides the mechanism: configure duty charges on the PO, allocate to PO lines by value, and post the allocation as an inventory cost adjustment. The duty payable goes to AP; the offsetting entry adjusts inventory. When the goods sell, the duty flows through COGS as part of the landed unit cost. Gross margin reflects the true economics of the business, not just the vendor invoice price.

⚠️ Dual-Use Items Shipped Without Export License — Revenue Reversed, Penalty Assessed

A technology manufacturer sells electronic components that have dual-use classification (ECCN 3A001 — specific electronic components with both commercial and military applications). A new sales order is entered for a customer in a destination that requires export license for these items. The order entry person isn’t trained on ECCN requirements; the sales order doesn’t trigger any system check because the item’s ECCN isn’t recorded in D365 and no country restriction rule is configured for this destination/product combination. The shipment proceeds. Revenue is recognized. Two months later, BIS (Bureau of Industry and Security) notifies the company of an unlicensed export of a controlled item. The revenue is reversed, a penalty is assessed, and the company enters into a settlement agreement requiring enhanced compliance procedures and a compliance audit covering the prior three years of export activity.

Fix: ECCN codes must be recorded on items in D365, and country/item restriction rules must be configured for all destination-product combinations requiring export licenses. This is not a post-go-live enhancement — it is a pre-production compliance requirement. For any company that manufactures or distributes items with potential dual-use classification, engage trade counsel to conduct an ECCN classification review of the product catalog before D365 go-live. Configure the classification results in D365’s foreign trade codes. Enable country restriction rules for controlled destinations. Integrate a restricted party screening solution at order entry. Export compliance is a legal obligation — “we didn’t know the item was controlled” is not a defense in an export enforcement action.

⚠️ FTA Certificates of Origin Not Tracked — Preferential Duty Rates Are Claimed Without Documentation

A US manufacturer exports goods to Mexico and Canada under USMCA (formerly NAFTA) preferential tariff rates. The sales team routinely includes a USMCA Certificate of Origin with export shipments, claiming preferential treatment. Finance doesn’t track whether the items actually qualify — whether the required regional value content and tariff shift rules are met. When a CBSA (Canada Border Services Agency) audit reviews three years of USMCA claims, eight product lines that were claimed as USMCA-originating don’t meet the product-specific rules. The preferential duty rates were improperly claimed. The importer (the Canadian customer) faces duty reassessments plus interest; the US exporter faces liability for providing false certificates of origin. The Canadian customer relationships suffer significantly.

Fix: USMCA (and any other FTA) Certificate of Origin must be supported by documented qualification analysis — not issued routinely on the assumption that products qualify. D365 supports country of origin tracking and FTA eligibility setup at the item and product level. Finance and trade compliance must maintain a qualification file for each product claiming preferential treatment: the product-specific rule of origin, the regional value content calculation, the bill of materials components and their origins, and the analysis supporting qualification. Review and update qualifications annually and whenever BOMs, suppliers, or sourcing countries change. Claiming preferential treatment without documentation is not just an accounting risk — it is a trade compliance violation with significant liability for both exporter and importer.

⚠️ Landed Cost Timing Mismatch — Duty Invoices Arrive After Inventory Has Sold

The freight broker’s customs duty invoice typically arrives 30–45 days after goods clear customs — well after the inventory has been received into D365 and sometimes after it has already been sold. Finance processes the duty invoice when it arrives, posting it as a landed cost adjustment. But the inventory it relates to was sold weeks ago — the landed cost adjustment posts to COGS in the current period, not the period in which the goods sold. If the goods cleared customs in Q3 and sold in Q3, but the duty invoice arrives and is posted in Q4, Q3 COGS is understated and Q4 COGS is overstated by the same amount. For high-import-volume businesses, the quarterly COGS distortion can be material.

Fix: For recurring import lanes with predictable duty rates, accrue estimated landed costs at the time of goods receipt rather than waiting for the broker invoice. The accrual entry (Dr Inventory / Cr Estimated Duty Payable) is estimated using the known tariff classification, the assessed value, and the applicable duty rate. When the broker invoice arrives, the actual duty replaces the estimate — reversing the accrual and posting the actual AP. For shipments where duty rates are uncertain or where goods are subject to tariff actions with retroactive rate changes, accrue conservatively and adjust when the actual duty invoice confirms the rate. The matching objective is to have the duty cost in inventory in the same period the goods receive — which means estimating before the broker invoice if the invoice timing lags receipt by more than a few days.

Do This / Don’t Do This

✓ Do This

- Populate commodity codes (HS/CN codes) on every item that will trade across EU borders before go-live

- Capitalize import duties, freight, and other directly attributable import costs into inventory cost — not period expense

- Use the correct allocation method per charge type — freight by weight/volume, duties by declared value

- Record ECCN codes on dual-use items and configure country restriction rules before any export orders are entered

- Accrue estimated landed costs at goods receipt when broker invoices will arrive after period end

- Track FTA certificate of origin qualifications with documented analysis — don’t issue certifications on assumption

- Monitor intra-EU trade value against national Intrastat thresholds before the first declaration period

- Integrate restricted party screening at order entry — not as a post-shipment check

- Engage trade counsel for ECCN classification review before D365 go-live for manufacturers of potentially controlled items

✗ Don’t Do This

- Treat commodity codes as a logistics data field — missing codes produce incomplete Intrastat declarations

- Expense import duties as incurred — COGS and gross margin will both be wrong for the entire product catalog

- Ship dual-use items to controlled destinations without first verifying export license requirement

- Issue FTA Certificates of Origin without documented product qualification analysis

- Wait for broker invoices before accruing landed costs — if goods have sold, the duty hits COGS in the wrong period

- Use a single landed cost allocation method for all charge types — freight logic and duty logic follow different bases

- Leave restricted party screening as a manual check by the export team — the volume and human error risk require system-level controls

Up Next:

Trade compliance addresses the boundary of the supply chain. The next post looks deeper into how D365 F&O manages the vendor relationship before goods even arrive: Vendor Collaboration and Advanced Procurement Workflows in D365 F&O — the vendor portal, purchase agreements and trade agreement pricing, requisition and procurement policies, consignment inventory accounting, and the three-way match controls that prevent AP from paying for what wasn’t received at the price that wasn’t agreed.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

Recent Blogs:

- Subscription and Recurring Revenue in D365 Business Central

- Financial Period Close Governance: The Financial Period Close Workspace in D365 F&O

- Cost Accounting in Business Central

- Cash Flow Forecasting in Business Central

- Electronic Reporting and Regulatory Submissions in D365 F&O

If this post helped you solve a real problem, please share it with a Finance colleague who is in the middle of an ERP implementation or a post-go-live optimization. If you have a topic that I haven’t covered, please reach out. There is always one more topic worth exploring.

Leave a Reply