How D365 F&O’s Revenue Recognition module implements the five-step model, contract setup with multiple performance obligations, transaction price allocation, variable consideration and constraint, contract modifications, and the five Revenue Recognition configuration failures that produce financial statement restatements.

The Five-Step Model—How D365 F&O Implements Each Step

ASC 606 / IFRS 15 Five-Step Model—D365 F&O Implementation

- Identify the Contract With a Customer

- A revenue recognition contract in D365 F&O is created from a sales order or a set of related sales orders. The Revenue Recognition module supports bundling multiple sales orders for the same customer into a single contract when the orders represent a single arrangement with multiple elements. Finance defines the contract identification criteria: which customer arrangements constitute a single contract for recognition purposes versus independent contracts.

- D365 Configuration: Revenue Recognition → Setup → Revenue recognition parameters. Define whether contracts are identified at the sales order level or require manual bundling of related orders.

- Identify the Performance Obligations in the Contract

- Performance obligations are the distinct goods or services the organization promises to deliver. D365 F&O identifies performance obligations at the item level—each item on a sales order can represent a separate performance obligation, or items can be bundled into a single obligation when they are not distinct on their own. Finance must define the performance obligation structure for each revenue-generating item category: is a software license a separate obligation from the implementation service that follows it? Is the product a separate obligation from the post-sale support contract?

- D365 Configuration: Released products → Revenue recognition FastTab. Assign each item an Item revenue recognition schedule (defines how recognition occurs: at point in time, over time, or per a custom schedule) and confirm whether the item is a standalone deliverable or must be bundled with related items.

- Determine the Transaction Price

- The transaction price is the amount Finance expects to receive for satisfying the performance obligations. For fixed-price arrangements, the transaction price is the contract price. For variable consideration arrangements—volume discounts, rebates, penalties, performance bonuses—Finance must estimate the variable amount using either the expected value method (probability-weighted average) or the most likely amount method, constrained to the amount for which a significant reversal of cumulative revenue is not probable.

- D365 Configuration: Revenue Recognition → Setup → Revenue price setup. Define standalone selling prices for each performance obligation. Configure variable consideration estimates and the constraint assessment methodology for each variable element.

- Allocate the Transaction Price to the Performance Obligations

- When a contract has multiple performance obligations, the total contract price is allocated to each obligation based on its relative standalone selling price (SSP). If the organization sells the software license alone for $120,000 and the implementation service alone for $80,000, a bundled contract priced at $180,000 would allocate $108,000 to the license (120/200 of $180,000) and $72,000 to the service (80/200 of $180,000)—regardless of how the contract is priced or invoiced. D365 F&O performs this allocation automatically using the SSPs Finance configures.

- D365 Configuration: Revenue Recognition → Periodic tasks → Revenue price allocation. Run after sales order creation to allocate the order’s transaction price across performance obligations. Finance must define SSPs for every item that participates in multi-element arrangements.

- Recognize Revenue When (or As) the Performance Obligation Is Satisfied

- Revenue is recognized when control of the promised good or service transfers to the customer—at a point in time (product delivery, license activation) or over time (subscription services, long-term contracts where the customer simultaneously receives and consumes the benefit). D365 F&O’s revenue recognition schedules define how the allocated transaction price moves from the Contract Liability (deferred revenue) account to the Revenue account as performance obligations are satisfied.

- D365 Configuration: Revenue recognition schedules define the recognition pattern (daily straight-line, milestone-based, usage-based, at point in time on confirmation). The schedule is assigned to the item and drives the Release revenue entries Finance posts when obligations are satisfied.

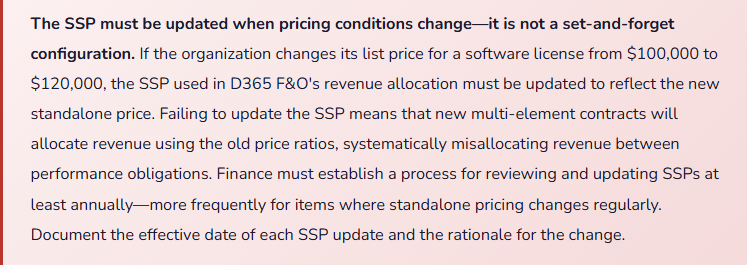

Standalone Selling Price—The Configuration Decision Finance Must Own Completely

The standalone selling price is the price at which the organization would sell a performance obligation separately to a customer. It is the allocation denominator for every multi-element contract and the most consequential configuration input in the Revenue Recognition module. Finance, not the implementation partner, must determine the SSP for each item that participates in bundled arrangements.

| SSP Estimation Method | When to Use | D365 F&O Configuration | Finance Documentation Required |

|---|---|---|---|

| Observable Price | The item is sold regularly on a standalone basis and a range of actual transaction prices is available. The SSP is the median or mode of standalone transaction prices within a reasonably narrow range. | Revenue price setup: enter the SSP as a fixed amount or range. When the contract price falls within the SSP range, no reallocation is required. | Quarterly analysis of standalone transaction prices confirming the SSP range remains representative. Document the data source (sales order history filtered to standalone sales) and the statistical method. |

| Adjusted Market Assessment | The item is not sold regularly on a standalone basis but comparable market prices for similar goods or services exist. The SSP is estimated from competitor pricing or market data, adjusted for the organization’s specific value proposition. | Revenue price setup: enter the estimated SSP based on the market assessment. Flag the item for Finance review when market conditions change materially. | Market assessment analysis documenting the comparable goods or services used, the sources of market pricing data, and the adjustments made for comparability. Updated when market pricing changes materially. |

| Expected Cost Plus Margin | The item has no observable market price. The SSP is estimated as the expected cost to deliver the item plus a reasonable margin consistent with the organization’s overall margin profile for similar products or services. | Revenue price setup: the SSP is calculated from cost data and a defined margin percentage. Finance must update the SSP when cost structures change. | Cost-plus model documenting the cost basis, the margin percentage applied, and the rationale for the selected margin. Updated when cost structures change materially. |

| Residual Approach | Permitted only when the SSP is highly variable (the item is sold across an extremely wide price range in different contracts) or highly uncertain (a new product with no pricing history). The residual SSP = total contract price minus the sum of all other observable SSPs. | Revenue price setup: designate the item as residual. D365 F&O will allocate the residual contract price to this item after allocating the other items at their configured SSPs. | Documentation of why the residual approach is justified—specifically, why the item’s SSP is highly variable or highly uncertain. The residual approach requires justification; it is not a default for items Finance has not priced. |

Contract Modifications—The Accounting Branch Decision D365 F&O Requires Finance to Make

A contract modification occurs when the parties agree to change the scope or price of an existing contract. ASC 606 and IFRS 15 require Finance to determine whether the modification creates a new contract, modifies the existing contract prospectively, or requires a cumulative catch-up adjustment—and D365 F&O’s contract modification functionality implements whichever accounting treatment Finance directs. The system will not make this determination automatically; Finance must analyze each modification and select the appropriate treatment.

New Separate Contract

The modification adds a distinct good or service at its standalone selling price. Treated as a new contract—the existing contract is not modified. D365 F&O: create a new sales order for the added scope. No adjustment to the original contract’s allocation.

Prospective Modification

The modification changes remaining performance obligations. Revenue not yet recognized is recalculated based on the modified terms. D365 F&O: modify the existing revenue recognition schedule going forward. Revenue recognized to date is not restated.

Cumulative Catch-Up

The modification affects obligations that are substantially the same as those already partially satisfied. Requires a catch-up adjustment to revenue recognized to date. D365 F&O: post a revenue adjustment entry reflecting the cumulative effect. Finance must calculate and document the catch-up amount.

Combination Approach

The modification has elements of both a new contract and a modification of existing obligations. Each element is accounted for under the appropriate branch. Finance documents which elements of the modification are treated as new contract and which as prospective modification.

Five Revenue Recognition Configuration Failures That Produce Restatements

⚠️ SSP Not Configured for Bundled Items—Revenue Allocated at Contract Price Instead of Relative SSP

The organization sells a software platform with a three-year support arrangement. The software license is priced at $90,000 in the contract. The support is priced at $30,000 per year ($90,000 total). The combined contract price is $180,000. When Finance configures the Revenue Recognition module, the items are added to the sales order but no standalone selling prices are entered in the Revenue price setup. D365 F&O, without SSPs to drive relative allocation, recognizes revenue at the line-item contract prices: $90,000 for the software license at delivery and $30,000 per year for support. If the organization’s standalone selling price for the license is $120,000 and the standalone SSP for support is $30,000 per year (total $210,000), the correct allocation of the $180,000 contract is $102,857 to the license and $25,714 per year to support. By not configuring SSPs and relying on contract prices, Finance is recognizing $90,000 for the license instead of $102,857—a $12,857 understatement of license revenue recognized at delivery and a corresponding overstatement of support revenue spread over three years.

Fix: SSP configuration is a prerequisite to activating the Revenue Recognition module for any multi-element arrangement. Before any bundled contract is entered into D365 F&O, Finance must have defined the SSP for every item that will appear in multi-element sales orders. The Revenue price setup must be complete for all relevant items before the module is used in production. After implementing the module, Finance runs the Revenue price allocation job (Revenue Recognition → Periodic tasks → Revenue price allocation) on each sales order to confirm allocation is occurring correctly before the order is confirmed. The first 20–30 multi-element contracts should be manually recalculated by Finance to validate that D365 F&O’s allocation matches the expected output.

⚠️ Revenue Recognition Schedule Set to Point-in-Time for Service Items—All Revenue Posts at Invoice

The organization provides annual subscription access to a software platform plus monthly professional services. The implementation team configures all items with a Point-in-Time recognition schedule because that was the default in the system template they used. Finance goes live. Every invoice posts revenue immediately at the invoice date. The subscription access—a service the customer receives continuously over 12 months—is recognized entirely in the invoicing period. A $240,000 annual subscription invoiced on January 1 is fully recognized in January. The professional services hours, delivered monthly throughout the year, are recognized when invoiced rather than as delivered. By March, the income statement shows front-loaded revenue that does not represent the pattern of service delivery. The auditor, reviewing the revenue recognition methodology at year-end, requires a restatement to recognize the subscription access ratably over 12 months and the professional services as the hours are delivered.

Fix: The revenue recognition schedule assigned to each item must reflect the actual pattern of performance obligation satisfaction—not the invoicing pattern or the default template. For subscription access and other over-time performance obligations, the schedule must be a straight-line ratable recognition over the service period (daily proration from contract start to contract end). For professional services billed on a time-and-materials basis, the recognition schedule must recognize revenue as the hours are incurred and approved, not at invoicing. Finance must review the recognition schedule for every item type before go-live and confirm it matches the accounting policy the organization has documented for each revenue stream. An item-by-item revenue recognition policy matrix (item type, recognition basis, recognition schedule in D365 F&O, ASC 606 basis) is the documentation Finance must maintain.

⚠️ Variable Consideration Not Constrained—Revenue Recognized Includes Amounts That Will Reverse

The organization’s contracts include a performance bonus: the customer pays an additional $50,000 if the implementation is completed in under 90 days. Finance configures the Revenue Recognition module to include the $50,000 bonus in the transaction price on contract inception because “we usually hit the deadline.” The $50,000 is allocated across the performance obligations and begins recognizing immediately. Of eight contracts configured this way in Q1, three miss the 90-day deadline and the bonus is forfeited. Finance must reverse $37,500 of revenue across three contracts in Q2 (the portions already recognized from the forfeited bonus). The reversal is a significant revenue reversal that the auditor characterizes as a failure to apply the variable consideration constraint—the amount was not constrained to the level for which a significant reversal was not probable, because the probability of forfeiture was material.

Fix: The variable consideration constraint must be applied to every variable element before it is included in the transaction price. The constraint question is: “Is it probable that including this amount will not result in a significant reversal of cumulative revenue when the uncertainty resolves?” For bonuses, penalties, and rebates, Finance must estimate the probability-weighted outcome and include only the amount that passes the constraint test. In D365 F&O, the constrained transaction price is what Finance enters as the revenue price for the contract—the unconstrained amount (the bonus) is not included in the transaction price until the uncertainty resolves. Finance must document the constraint assessment for each material variable consideration element and review it at each reporting date as additional information about the probability of outcome becomes available.

⚠️ Contract Modification Treated as Prospective When Catch-Up Was Required

The organization is midway through a large implementation contract priced at $600,000. At the six-month mark, the customer and the organization agree to add additional scope for $80,000. Finance treats the modification as a prospective change (new scope at SSP, separate contract treatment) because it is cleaner to handle. The correct analysis is that the additional scope is not distinct—it is closely related to the work already partially performed, and the modification should be accounted for as a modification of the existing contract with a cumulative catch-up. Under the correct treatment, the total transaction price increases to $680,000 and the revenue recognized to date must be recalculated based on the updated estimate of completion percentage applied to the full $680,000. Finance’s choice of prospective treatment understates revenue for the current period (because the catch-up adjustment was not recognized) and will overstate revenue in future periods (because the remaining $80,000 will be recognized prospectively over the remaining performance obligation rather than partially catch-up now).

Fix: Every contract modification requires a documented accounting analysis before the modification is entered in D365 F&O. The analysis must address: is the added scope distinct? Is the additional price the SSP of the added scope? Based on the answers, which accounting branch applies? Finance should maintain a contract modification log for every material contract modification: the contract, the modification date, the modification description, the accounting analysis, the treatment selected, and the Finance approver. The log is the audit trail that supports the modification accounting. For high-volume contract environments, Finance should develop a standard modification analysis template that guides the branch determination consistently across all modifications.

⚠️ Release Revenue Job Not Run at Period End—Contract Liability Balance Grows While Revenue Understates

D365 F&O’s Revenue Recognition module creates a Contract Liability (deferred revenue) balance when an invoice is posted and the performance obligation has not yet been satisfied. Revenue is transferred from the Contract Liability to the Revenue account when Finance runs the Release revenue periodic job (Revenue Recognition → Periodic tasks → Release revenue). The Release revenue job must be run at each period end—or more frequently for time-based recognition schedules—to post the recognition entries. Finance goes live with the Revenue Recognition module. The Release revenue job is not on the period-close checklist. For three months, invoices post to Contract Liability but the Release revenue job is never run. Revenue is materially understated; the Contract Liability account balance grows to $1.2 million. The auditor reviews Q3 revenue and asks why Contract Liability increased without corresponding revenue recognition. Finance discovers the Release revenue job has never been run and must post three months of recognition entries in Q4 to correct the cumulative understatement.

Fix: The Release revenue job is a period-close requirement for every organization using the Revenue Recognition module. It belongs on the close checklist between “post all invoices for the period” and “reconcile deferred revenue to the revenue recognition schedule.” Finance must run the job at least monthly (more frequently for daily-proration arrangements where the balance should reflect recognition through the last day of the period) and review the resulting GL entries to confirm the recognition amounts match the expected schedule progression. The Contract Liability account balance after the Release revenue job is run should equal the unearned portion of all open contracts—Finance should reconcile this balance to the open contract revenue recognition schedules at each period end as part of the deferred revenue reconciliation.

Do This / Don’t Do This

Do This

- Document the accounting policy for each revenue stream before configuring D365 F&O—the module implements whatever Finance configures

- Configure SSPs for every item in multi-element arrangements before the first bundled contract is entered

- Review and update SSPs at least annually and when standalone pricing changes materially

- Run the Revenue price allocation job on the first 20–30 multi-element contracts post-go-live to validate allocation output

- Apply the variable consideration constraint to every variable element before including it in the transaction price

- Document every material contract modification with an accounting analysis before entering it in D365 F&O

- Add the Release revenue job to the period-close checklist and reconcile the Contract Liability balance to open recognition schedules monthly

Don’t Do This

- Delegate the accounting policy decisions to the implementation partner—they can configure the system but cannot make the recognition policy choices

- Default all items to Point-in-Time recognition without confirming it matches the actual performance obligation satisfaction pattern

- Include unconstrained variable consideration in the transaction price because “we usually hit the target”

- Treat contract modifications as prospective for convenience without performing the branch determination analysis

- Leave the Release revenue job off the close checklist—it does not run itself

- Set SSPs once at implementation and never update them as pricing evolves

- Accept the implementation partner’s default template configurations without Finance review of each item’s recognition schedule

What’s Next:

Revenue recognition addresses when revenue hits the income statement. The next post addresses a daily Finance operational process that either runs precisely or creates close-time chaos: Advanced Bank Reconciliation and Cash Application Automation in D365 F&O—the advanced bank reconciliation workspace, the matching rule configuration Finance must design, the cash application automation options for high-volume AR environments, how to govern the exception queue that automated matching inevitably produces, and the five bank reconciliation failures that turn a 30-minute close task into a three-day investigation.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

If this post helped you solve a real problem, share it with a Finance colleague who is in the middle of an ERP implementation or a post-go-live optimization. If you have a topic that I haven’t covered, please reach out. There is always one more post worth writing.

Interesting in learning more about D365? Here are some of my latest posts:

Leave a Reply