How manufacturing companies must configure BC’s costing, production order accounting, and inventory valuation differently from distribution and service businesses, the WIP accounting mechanics Finance must understand even when Operations runs production, the standard cost update process Finance must own annually, and the five manufacturing Finance configuration failures that produce cost variances Finance cannot explain to the auditor.

Choosing the Costing Method for Manufacturing Items—Finance’s Most Consequential Decision

The costing method on each manufactured item determines how BC calculates the cost of produced goods and how production cost variances are handled. Finance must own this decision—not the production planner or the BC implementation consultant—because the costing method determines the income statement treatment of manufacturing cost differences for the item’s entire life in BC.

Standard Cost

Each manufactured item carries a predetermined standard cost—the expected cost to produce one unit based on standard material quantities, standard labor hours, and standard overhead rates. When production output is posted, inventory increases at the standard cost. Differences between actual production costs and the standard cost post to variance accounts. The income statement shows the standard cost of goods sold; variances are reported separately.

Best for: Companies with stable production processes and consistent material costs, where variance analysis is a meaningful management tool. Standard costing makes budget-vs-actual analysis straightforward: actual cost deviations appear as variances that Finance can investigate by type (material, labor, overhead).

Finance owns: Annual standard cost update. If material prices change materially mid-year, Finance must evaluate whether a mid-year standard update is required. Outdated standards accumulate as purchase price variances that distort COGS.

Average Cost

The average cost of all inventory on hand is recalculated after each receipt. Produced items are valued at the weighted average of their production cost components at the time of production completion. COGS uses the average cost at the time of sale.

Best for: Companies with high transaction volumes and interchangeable components where tracking individual cost layers is impractical. Average costing smooths cost fluctuations without requiring a standard cost update process.

Finance owns: The Adjust Cost—Item Entries batch must run regularly (daily or at each period close) to finalize actual costs from production and purchasing. Before the batch runs, some item ledger entries carry expected costs. Finance must run the batch before the period-end inventory reconciliation or the numbers will not agree.

FIFO

The cost of the oldest inventory layer is used first when items are consumed in production or sold. Each production receipt creates a cost layer at the actual production cost; consumption draws from the oldest open layer.

Best for: Companies where the cost of specific production runs is meaningful and where older inventory should be consumed and valued before newer inventory. FIFO produces a balance sheet inventory value that reflects recent production costs (newer cost layers remain on hand).

Finance owns: FIFO costing layers must be understood when analyzing inventory valuation differences between reporting periods. A FIFO inventory balance that appears to have changed dramatically may reflect that an old, low-cost layer was consumed rather than that production costs changed.

Specific Cost

Each individual unit carries its own specific production cost, identified by lot or serial number. Appropriate for high-value, individually produced items where each unit’s cost must be tracked independently: custom machinery, bespoke products, items with significant material cost variation between production runs.

Best for: Low-volume, high-value production where each unit is traceable and its specific cost is material to margin analysis. Lot and serial tracking must be maintained on every production transaction for Specific costing to work correctly.

Finance owns: Lot and serial tracking discipline. Any production posting without a lot or serial number cannot be correctly costed under Specific costing. Finance must confirm with Operations that tracking is maintained on 100% of production transactions.

Production Order WIP Accounting—What Finance Must Understand Even When Operations Runs It

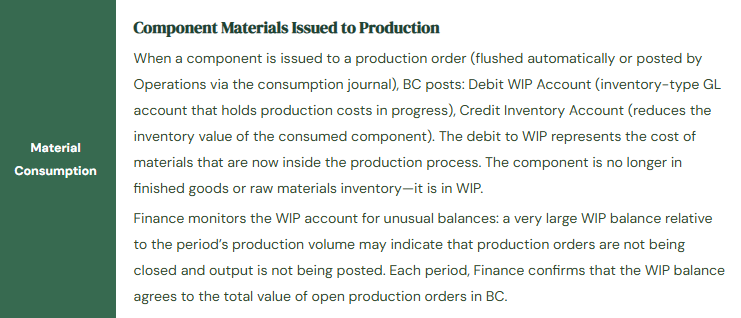

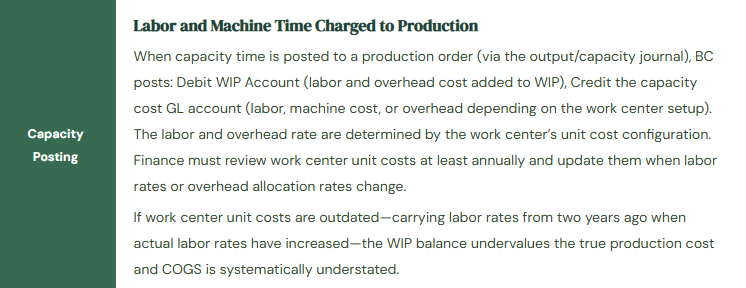

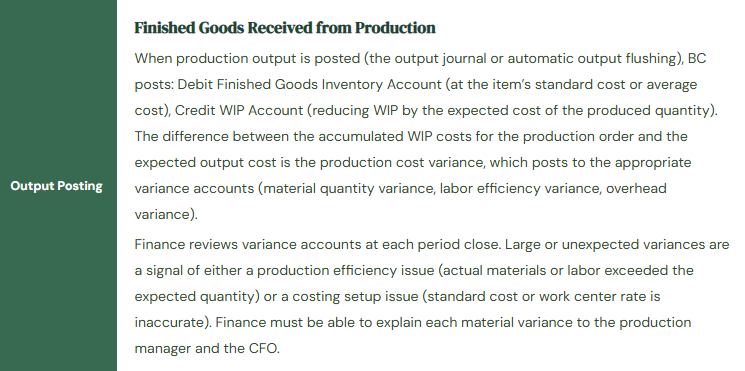

When a production order is created and released in BC, costs accumulate on it as materials are issued and capacity (labor and machine time) is consumed. These costs are captured in BC’s WIP (Work in Progress) accounting layer until the production order is finished and output is posted. Finance must understand how this accounting works because the WIP balance on the balance sheet represents real production cost, and Finance is accountable for reconciling it at period end.

Production Order WIP Accounting—GL Posting Pattern Finance Must Understand

Five Manufacturing Finance Configuration Failures

⚠️ Standard Costs Not Updated at Year-End—Purchase Price Variances Accumulate All Year

The organization uses standard costing for manufactured items. Standards were set at BC go-live using material costs from the prior year. Commodity prices for two key raw materials have increased by 18% and 22% respectively during the year. Every purchase receipt for these materials posts a purchase price variance (actual cost minus standard cost) to the Purchase Price Variance account. By year-end, the Purchase Price Variance account has a £340,000 debit balance. Ending inventory is valued at the understated original standards. COGS for the year is also understated because sales consumed inventory at the original standard cost rather than at the actual higher cost. Both the balance sheet (inventory undervalued) and the income statement (COGS understated, gross margin overstated) are materially misstated. The auditor asks for the standard cost update documentation and finds none exists for the year.

Fix: Standard cost updates are an annual Finance accounting event, not an optional system task. Finance plans the standard cost update as part of the year-end calendar: in Q4, Finance collects the updated material costs for the coming year from procurement (the expected purchase prices based on supplier quotes and contracts), updates the unit costs in BC’s Standard Cost Worksheet, rolls up the updated standards to all manufactured items that use the updated components, reviews the revaluation amount that BC calculates (the adjustment to on-hand inventory from old standard to new standard), and posts the revaluation journal before the new year begins. The revaluation posting moves the on-hand inventory from the old standard to the new standard and posts the adjustment to the Inventory Revaluation account. Finance reviews the revaluation amount for reasonableness before posting—it should reflect the known cost changes during the year.

⚠️ WIP Account Balance Not Reconciled—£280,000 of Finished Production Still in WIP

Finance does not run the WIP reconciliation at period end. Over six months, production orders for 14 items have been marked as Finished in BC but the output posting for those orders was never completed—Operations finished the production orders in the production planning module without posting the output to the Finished Goods inventory. BC marks the orders as Finished but does not automatically clear the WIP balance when output has not been posted. The WIP account carries £280,000 of production costs for orders that Operations considers complete. The Finished Goods inventory is £280,000 lower than it should be. Finance’s balance sheet shows £280,000 of WIP that does not represent active in-progress production. When the auditor asks Finance to reconcile the WIP account balance to the open production orders report, Finance cannot explain the £280,000 discrepancy.

Fix: The WIP reconciliation is a monthly period-close procedure. Finance runs the Open Production Orders report filtered to orders with WIP posted and compares the total WIP value on the report to the WIP GL account balance. The two should agree. Any difference represents either WIP on finished orders (output not posted) or WIP on orders not shown in the report (data entry errors in order status). Finance investigates every WIP discrepancy before the period closes. For the 14 orders with unposted output, Finance works with Operations to determine the correct output quantity and posts the output journal before the period is locked. If Operations cannot determine the correct output quantity for historical orders, Finance estimates based on the BOM quantity and actual material consumption and documents the estimate as an accounting judgment.

⚠️ Work Center Unit Costs Not Updated—Labor Rates Two Years Out of Date

The organization’s two work centers were configured at go-live with labor rates of £28 per hour and £35 per hour based on the payroll cost per hour at the time of implementation. Two years later, pay increases and employer cost increases have raised the actual labor cost to £34 per hour and £43 per hour respectively. Nobody has updated the work center unit costs in BC. Every production order posted in the last two years has charged labor to WIP at the old rates. The WIP balance for in-progress orders understates actual labor cost by 21% on average. COGS for all produced and sold items is understated by the same proportion of the labor cost component. Finance has been reporting gross margins that are £15,000–£20,000 higher than actual per month for two years. The variance between actual gross margin and the margin Finance has been reporting to management is discovered when a detailed product costing exercise is undertaken for a pricing decision.

Fix: Work center unit cost review is an annual Finance task, aligned with the payroll budget cycle. Each year, Finance reviews the work center unit costs in BC (Manufacturing → Setup → Work Centers → Unit Cost fields) and updates them to reflect: direct labor cost per hour (from the payroll budget), plus employer costs (National Insurance, pension, benefits as a percentage), divided by the expected productive hours per period. Finance documents the calculation each year and retains it as the costing rate justification. If labor costs change materially mid-year (significant pay award, headcount change affecting the overhead rate), Finance assesses whether a mid-year work center cost update is required and posts the update with an effective date. The standard cost rollup is re-run after any work center cost update to update the standard cost of all manufactured items that use the affected work centers.

⚠️ Production Output Posted to Wrong Finished Goods Account—Manufactured Items in Raw Materials on Balance Sheet

During implementation, the inventory posting setup for the manufactured items posting group was configured to use the Raw Materials inventory account (GL 3100) instead of the Finished Goods inventory account (GL 3200). The error was not caught during UAT because the test production orders used a different item category that had the correct posting setup. In production, all manufactured item output posts to GL 3100. The balance sheet shows Raw Materials inflated by the value of all manufactured output and Finished Goods at zero. Finance runs the inventory valuation report and observes that manufactured items appear in the Raw Materials balance but attributes it to BC’s categorization rather than a posting error. The auditor, reviewing the inventory reconciliation, notices that the value in GL 3100 includes items classified as Manufactured in BC’s item master and flags the posting group misconfiguration.

Fix: Inventory posting setup for manufactured items must be validated by Finance before any production output is posted in the live environment. Finance opens the Inventory Posting Setup page in BC and confirms for each combination of Location Code and Inventory Posting Group: the Inventory Account is the correct balance sheet account for that item category (Finished Goods for manufactured items, Raw Materials for purchased components, WIP for in-progress items), and the WIP Account is configured and points to the correct WIP balance sheet account. Finance runs a test production order in the UAT environment, posts material consumption, posts capacity, posts output, and closes the order—then traces every GL posting to the correct accounts. This test takes two hours and prevents the posting account error from propagating into the live environment.

⚠️ Adjust Cost—Item Entries Batch Not Run—Inventory Valuation and COGS Are Both Wrong at Period End

The organization uses Average costing for manufactured items. The Adjust Cost—Item Entries batch is configured to run as a scheduled job but the job queue entry was inadvertently deactivated when IT made changes to the BC job queue three months ago. For three months, no cost adjustments have run. Produced items carry expected costs at the time of output posting rather than actual finalized costs from the production orders. Purchase receipts that arrived after the last cost adjustment run have not updated the average cost. The inventory valuation report total differs from the GL inventory account balance by £48,000—the accumulated cost adjustments that should have posted but did not. Finance discovers the gap when running the period-end inventory reconciliation and cannot determine whether the £48,000 is a reconciliation error or a cost adjustment backlog.

Fix: Finance confirms the Adjust Cost—Item Entries job queue entry is active and running on schedule immediately after any BC update, any IT maintenance on the job queue, and at each period close. The confirmation takes two minutes: Finance opens the Job Queue Entries page, finds the Adjust Cost—Item Entries entry, and confirms Status = Ready and the Next Run Date/Time is in the near future. Finance also monitors the output: after each scheduled run, the entry should show Last Status = Success and a recent Last Run Date. A job queue entry showing Last Status = Error or a Last Run Date that is many days in the past indicates the job has stopped running and requires Finance to investigate and restart it. The period-end close checklist includes: confirm Adjust Cost batch ran successfully for the period before running the inventory reconciliation.

Do This / Don’t Do This

Do This

- Finance must own the costing method decision for manufactured items—it determines how COGS behaves for the item’s entire BC life

- Run the WIP reconciliation (WIP account vs. open production orders) at every period close

- Update standard costs annually and mid-year when material costs change materially

- Review work center unit costs annually, aligned with the payroll budget cycle

- Validate inventory posting setup for manufactured items in UAT before any production output is posted in the live environment

- Confirm the Adjust Cost batch is running successfully after every BC update and at each period close

- Review variance accounts (purchase price variance, labor efficiency variance, overhead variance) at every period close—material variances require explanation

Don’t Do This

- Delegate the costing method decision to the production planner or the implementation consultant without Finance involvement

- Skip the WIP reconciliation during busy closes—WIP discrepancies found monthly are hour-level problems; found at year-end audit they are day-level problems

- Leave standard costs unchanged for more than a year without reviewing whether they still reflect actual production costs

- Allow work center labor rates to remain at go-live values indefinitely—they become systematically inaccurate with every pay change

- Ignore the Adjust Cost batch status in the job queue—a deactivated batch means inventory and COGS are both wrong

- Accept large variance account balances as “normal for manufacturing” without investigating their root cause

Up Next:

Manufacturing Finance configuration covers the production cost cycle. The next post addresses the topic that affects every BC user in the organization but is rarely explained clearly to Finance teams: BC Licensing, User Types, and What Finance Must Know About Costs—how BC’s licensing model works, which user type Finance should specify for each Finance role, what the license cost implications are of common Finance configuration decisions (approval workflow users, Power Automate connections, external accountant access), and the five licensing decisions that generate unexpected Microsoft invoices Finance did not budget for.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

If this post helped you solve a real problem, share it with a Finance colleague who is in the middle of an ERP implementation or a post-go-live optimization. If you have a topic that I haven’t covered, please reach out. There is always one more post worth writing.

If you are interested in learning more, below are a few of my latest posts:

Leave a Reply