How D365 F&O’s consolidation framework aggregates multiple legal entity trial balances, the elimination rules that strip intercompany transactions from the consolidated view, currency translation for foreign subsidiaries under ASC 830 and IAS 21, and the reconciliation controls that make the consolidated financial statements auditable—not just arithmetically correct.

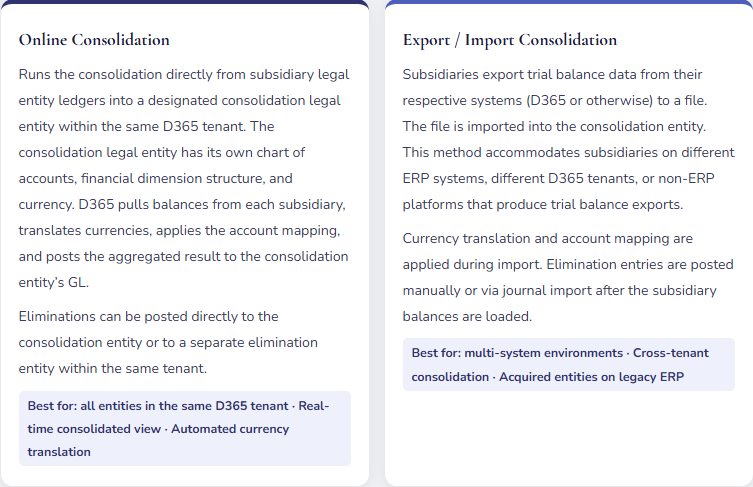

The Two Consolidation Methods in D365 F&O—Which One You Should Be Using

D365 F&O supports two consolidation approaches. Understanding the difference is the first decision Finance makes when designing the consolidation process.

Account Mapping—The Bridge Between Subsidiary and Consolidation Charts

Unless every subsidiary uses exactly the same chart of accounts as the consolidation entity, Finance must configure account mapping rules: for each subsidiary, which subsidiary GL account maps to which consolidation entity account. A subsidiary that uses account 6100 for Rent Expense maps to the consolidation entity’s 6200 (or whatever the consolidated chart uses for Occupancy Expense). The online consolidation process applies the mapping automatically during each consolidation run.

Account mapping in D365 is configured in the consolidation legal entity under General ledger → Consolidate → Account group mapping. The mapping is defined by source legal entity and source account range, pointing to the destination consolidation account. Finance must audit the account mapping completeness before the first consolidation run: every subsidiary account that carries a balance must map to a consolidation account. Unmapped accounts either fail during consolidation (if D365 is configured to require mapping) or post to a catch-all account that Finance discovers only when the consolidated trial balance shows a line nobody recognizes.

Currency Translation—What D365 Does and What Finance Must Configure

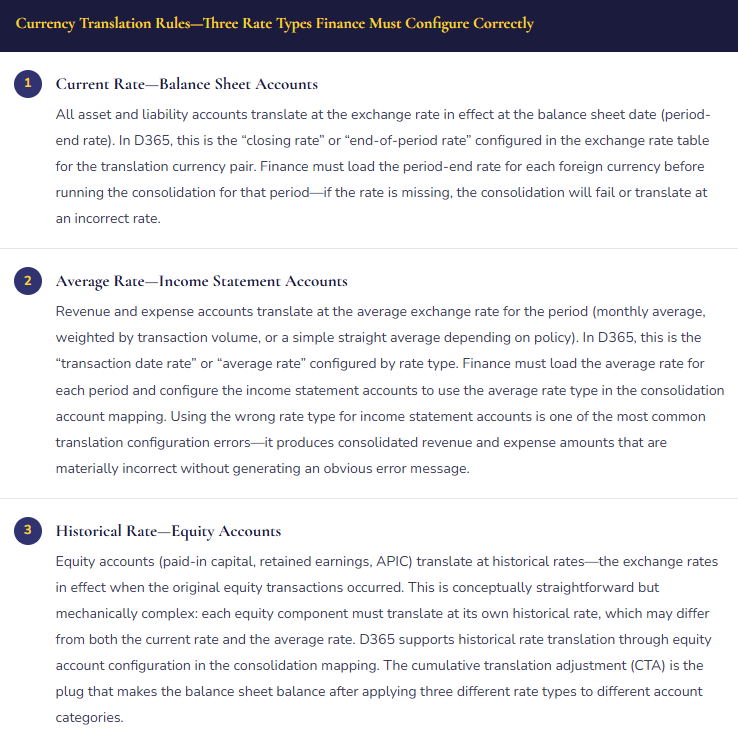

For subsidiaries with a functional currency different from the consolidation entity’s reporting currency, D365 applies currency translation during the consolidation run. The translation method follows ASC 830 (US GAAP) or IAS 21 (IFRS), both of which use the same mechanical approach:

The CTA ($13,500) is not an error—it is the mathematical consequence of translating different account categories at different rates. It accumulates in Other Comprehensive Income (OCI) on the balance sheet and is recycled to the income statement when the subsidiary is sold or liquidated.

Intercompany Eliminations—What Must Be Removed and How D365 Does It

When Entity A sells goods to Entity B, the sale is revenue in Entity A’s entity-level P&L and an expense (or inventory cost) in Entity B’s books. At the consolidated level, this transaction never happened—it is an internal movement of value within the group that should not appear in consolidated revenue or expense. Intercompany eliminations remove these cross-entity transactions so the consolidated financial statements reflect only transactions with external third parties.

| Intercompany Activity | Entity A Books | Entity B Books | Elimination Entry Required |

|---|---|---|---|

| Intercompany sale of goods | Revenue: $200,000 AR—Intercompany: $200,000 | Inventory/COGS: $200,000 AP—Intercompany: $200,000 | Dr. Intercompany Revenue $200,000 Cr. Intercompany COGS/Inventory $200,000 Dr. AP—IC $200,000 / Cr. AR—IC $200,000 |

| Management fee charged by parent to subsidiary | Revenue: $50,000 AR—Intercompany: $50,000 | Mgmt fee expense: $50,000 AP—Intercompany: $50,000 | Dr. Intercompany Revenue $50,000 Cr. Intercompany Management Fee Expense $50,000 Dr. AP—IC $50,000 / Cr. AR—IC $50,000 |

| Intercompany loan (parent to subsidiary) | Note Receivable—IC: $1,000,000 Interest Income—IC: $40,000 | Note Payable—IC: $1,000,000 Interest Expense—IC: $40,000 | Dr. Note Payable—IC $1,000,000 / Cr. Note Receivable—IC $1,000,000 Dr. Interest Income—IC $40,000 / Cr. Interest Expense—IC $40,000 |

| Intercompany dividend from subsidiary to parent | Dividend income: $75,000 Cash: $75,000 | Retained Earnings (dividend paid): $75,000 Cash: $75,000 | Dr. Dividend Income $75,000 Cr. Retained Earnings $75,000 (restores equity to pre-dividend balance for consolidation purposes) |

In D365 F&O, eliminations can be configured as automatic elimination rules under the consolidation legal entity. Rules are defined by account combination: when Entity A’s intercompany AR account is eliminated against Entity B’s intercompany AP account during consolidation, D365 generates the offsetting entries automatically. This requires that intercompany accounts are set up symmetrically—the same account code (or properly mapped accounts) used on both sides of every intercompany transaction.

Five Mistakes That Break the Consolidated Close

⚠️ Intercompany Accounts Not Set Up Symmetrically—Every Elimination Requires Manual Adjustment

When two entities were implemented at different times, the intercompany account structure was set up independently. Entity A uses account 1330 for intercompany receivables. Entity B uses account 1310 for intercompany payables. The account numbers are different. The elimination rules are configured to offset account 1330 against account 1310. But the entity C acquisition six months later added intercompany activity recorded to account 1340 in the new entity and account 1320 in the existing entity. Nobody updated the elimination rules. At consolidation, the 1340/1320 intercompany activity has no elimination rule and flows into the consolidated statements as if it were third-party revenue and expense. The consolidation team discovers unexplained intercompany balances in the consolidated trial balance and spends two days tracing them manually.

Fix: Establish an intercompany account policy before the first entity goes live and enforce it for every subsequent entity. The policy defines: the specific account codes used for intercompany receivables, intercompany payables, intercompany revenue, intercompany expense, and intercompany loans—and requires that the same account codes (or explicitly mapped equivalents) be used in every legal entity. Every time a new entity is added to the D365 environment, the intercompany account setup and elimination rules are reviewed and updated as part of the entity onboarding process. The elimination rules in the consolidation entity are tested with a sample intercompany transaction before the entity’s first consolidation cycle.

⚠️ Wrong Exchange Rate Type on Income Statement Accounts—Consolidated Revenue Is Misstated

The consolidation account mapping for the EUR subsidiary’s income statement accounts is configured to use the “closing” rate type instead of the “average” rate type. For the first three quarters, the EUR/USD rate is relatively stable and the difference is immaterial—nobody notices. In Q4, the EUR appreciates significantly. The closing rate at December 31 is 1.12; the average rate for Q4 is 1.07. Translating twelve months of EUR revenue at the December 31 closing rate instead of the monthly average rates overstates consolidated USD revenue by $680,000. The external auditor’s currency translation test computes the expected USD revenue using average rates and finds a $680,000 discrepancy. The configuration error has been present since go-live but was immaterial in stable rate periods—a rate move made it audit-significant.

Fix: The rate type configuration in the consolidation account mapping must be reviewed against the organization’s translation policy before the first consolidation run and tested by comparing the D365 translation output to a manual calculation using the correct rates. For US GAAP (ASC 830) and IFRS (IAS 21): assets and liabilities use the closing rate; revenues and expenses use the average rate (or the rate at the transaction date when translation at an average is not reasonable); equity components use historical rates. These three rate types should each be configured as distinct rate type codes in D365’s exchange rate setup, with the mapping in the consolidation setup pointing each account category to the correct rate type. Test the output quarterly in the first year—don’t wait for the annual audit to verify translation is correct.

⚠️ Intercompany Reconciliation Not Done Before Consolidation Runs—Elimination Differences Require Post-Close Adjustment

The consolidation closes every month on day seven of the following month. The intercompany reconciliation process—comparing each entity’s IC receivable and payable balances before the consolidation run—was designed to happen on day five. In practice, the subsidiaries are slow to close and the intercompany reconciliation gets compressed into two hours on day six. Three intercompany balances are unreconciled: a $28,000 management fee that Entity A recorded in March and Entity B didn’t accrue until April, a $12,000 timing difference on an intercompany inventory transfer, and a $6,000 rounding difference from a foreign currency transaction. The consolidation runs with these unreconciled differences. The consolidated trial balance has three unexplained residual intercompany balances. The CFO asks about them. Finance prepares manual post-close adjustments. The consolidation is amended. The timeline for the management report slips two days.

Fix: The intercompany reconciliation must be completed and signed off before the consolidation run executes—not compressed into the hours before the consolidation deadline. The IC reconciliation process: each entity produces an intercompany balance report by counterparty entity. Group Finance or the consolidation accountant compares each bilateral pair (Entity A’s receivable from B versus Entity B’s payable to A). Any difference greater than a defined threshold (typically the lesser of a dollar amount or a percentage of the balance) is escalated to the relevant entity controllers for same-day resolution. The consolidation run is a gate that does not open until the intercompany reconciliation sign-off is received. Building a hard gate into the close process calendar—rather than treating it as a best-effort step—is what makes this control operate consistently.

⚠️ CTA Account Is Unexplained and Growing—Three Years of Translation Errors Accumulated in OCI

The consolidated balance sheet has a Cumulative Translation Adjustment balance in OCI that has grown from $140,000 at the first consolidated close to $2.1 million over three years. Nobody has explained the growth. When the external auditor requests the CTA rollforward, Finance produces a summary: “Net translation adjustments per consolidation run.” The auditor asks for the calculation supporting the CTA amount for each period. Finance cannot produce it—D365 generated the number and Finance accepted it. The auditor’s own translation test produces a CTA balance $380,000 lower than D365’s. The difference is traced to the functional currency assignment of the German subsidiary—it was designated as USD functional currency at setup (incorrect) instead of EUR, causing D365 to apply remeasurement rules (ASC 830 “temporal method”) instead of translation rules for three years.

Fix: The CTA balance should be reconciled and explained at every consolidated period close, not accepted as a system-generated number without analysis. The reconciliation: beginning CTA balance plus current period translation adjustment (computed manually using the rate change and the subsidiary’s beginning net asset position) should approximate the ending CTA balance. Material differences require investigation. The functional currency designation for each entity must be documented and reviewed at entity setup and after any significant change in the subsidiary’s operating environment—a subsidiary that primarily operates, sells, and incurs expenses in EUR is an EUR functional currency entity regardless of the parent’s USD reporting currency. Functional currency is an accounting judgment, not a system default to be accepted without analysis.

⚠️ Consolidation Entity Chart of Accounts Has Gaps—Subsidiary Accounts Map to the Wrong Consolidated Line

The consolidation entity chart of accounts was designed when the group had two subsidiaries. A third subsidiary was acquired eighteen months later with a different industry structure and different account categories—specifically, it has a significant Other Income account (account 7800) that doesn’t exist in the original consolidation chart. The implementation team mapped account 7800 to the closest available account in the consolidation chart: 7900 (Miscellaneous Income). The subsidiary’s $1.8M of annual rental income from investment properties now appears in consolidated Miscellaneous Income rather than Other Income. The consolidated financial statement presentation is incorrect. The auditor asks why rental income from the subsidiary is classified as miscellaneous. Finance cannot provide a clean answer because the mapping was done by an implementation team member who is no longer with the firm.

Fix: The consolidation entity chart of accounts and account mapping must be reviewed whenever a new entity is added to the consolidation group—not just at initial implementation. The review asks: does every material account in the new entity have a corresponding consolidation account that correctly represents its financial statement classification? If gaps exist, add the appropriate accounts to the consolidation chart before the first consolidation run that includes the new entity. The account mapping documentation should be maintained as a permanent reference document with a history of changes and the rationale for each mapping decision. When the person who made a mapping decision leaves the organization, the rationale should be in the documentation, not in their head.

Do This / Don’t Do This

Do This

- Establish an intercompany account policy before the first entity goes live and enforce it for every entity added thereafter

- Complete and sign off the intercompany reconciliation before every consolidation run—it is a gate, not a best-effort step

- Configure three distinct rate types for currency translation: closing rate for balance sheet, average rate for income statement, historical rate for equity

- Test translation output against a manual calculation in the first year—don’t wait for the annual audit

- Document functional currency designation for each entity with supporting analysis—it is an accounting judgment, not a system default

- Reconcile and explain the CTA balance at every consolidated period close

- Review consolidation account mapping and elimination rules whenever a new entity joins the consolidation group

- Maintain account mapping documentation as a permanent reference with rationale for each mapping decision

Don’t Do This

- Set up intercompany accounts independently in each entity without a group-wide policy—elimination rules will fail for every asymmetric pair

- Accept the CTA balance as a system-generated number without reconciling it to a manual calculation—three years of translation errors are invisible until the auditor finds them

- Configure income statement accounts to translate at the closing rate—average rate is required and the difference is material when rates move

- Run the consolidation with unreconciled intercompany differences and plan to adjust afterward—post-close adjustments to consolidated statements undermine the integrity of the close process

- Add a new entity to the consolidation without reviewing account mapping completeness

- Accept the functional currency designation at setup without documented analysis—incorrect functional currency produces three years of remeasurement entries instead of translation entries

Up Next:

Consolidation closes the multi-entity Finance arc. The next post steps outside the D365 F&O core application and looks at the surrounding ecosystem: Power Platform Integration—Power Automate, Power Apps, and Power BI with D365 F&O—how Finance uses each tool, what connects them to D365 data, the governance considerations that keep the Power Platform from becoming a shadow IT layer outside Finance’s visibility, and the practical use cases that actually reduce manual work rather than just adding another dashboard nobody maintains.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

Recent Posts:

- AI and ERP Security: What Copilot Means for Your D365 Security Roles and Internal Controls

- The Natural Language ERP: Stop Running Reports, Start Asking Questions

- AI Adoption in ERP: Why Change Management Is Your Most Critical AI Investment

- Agent 365: Microsoft’s Control Tower for All Your ERP Agents

- AI in D365 Supply Chain: From Demand Planning to Warehouse Intelligence

If this post helped you solve a real problem, please share it with a colleague who is in the middle of an ERP implementation or a post-go-live optimization. If you have a topic that I haven’t covered, please reach out. There is always one more topic worth exploring.

Leave a Reply