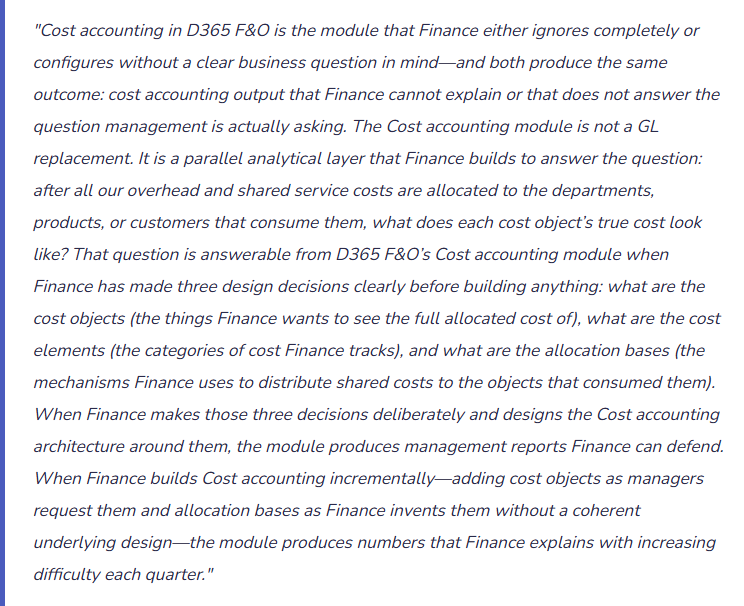

How D365 F&O’s Cost accounting module provides a second, allocation-enriched view of the organization’s cost structure alongside the statutory GL, the cost object and cost element architecture Finance must design before configuring, the allocation policy Finance must own as an accounting decision, and the five cost accounting failures that produce management reports Finance cannot use to make the decisions the module was designed to support.

The Four Architecture Components Finance Must Design Before Configuring

Cost Objects

The things Finance wants to see the full allocated cost of—the “what did it really cost to…” question. Cost objects can be cost centers (departments), profit centers (business units or product lines), projects, products, or customers. D365 F&O’s Cost accounting module supports any dimension as a cost object dimension.

Finance designs: Which dimensions from the GL financial dimension structure become cost object dimensions in Cost accounting. A department dimension in the GL can become the cost center cost object dimension in Cost accounting, making each department a cost object whose direct and allocated costs Finance tracks separately.

Critical pre-configuration question: What management decisions will the cost object cost structure support? If management wants to know the full cost of each product line, the product line dimension must be the cost object dimension. If management wants department-level cost responsibility, the department dimension must be the cost object. Finance cannot answer both questions with a single cost object dimension—multi-dimensional cost analysis requires multi-dimensional cost object configuration.

Cost Elements

The categories of cost that flow into Cost accounting from the GL—the “what kind of cost” dimension. Cost elements correspond to GL accounts: the Salaries GL account becomes the Salaries cost element, the Rent GL account becomes the Facilities cost element. Cost elements can be grouped into a cost element hierarchy for reporting purposes (Personnel costs = Salaries + Benefits + Employer contributions).

Finance designs: The mapping between GL accounts and cost elements. Not every GL account needs to be a separate cost element—Finance groups related accounts into meaningful cost elements at the level of granularity that supports the management reporting requirements. Too many cost elements produce cost reports that are difficult to read and discuss; too few collapse cost categories that management needs to distinguish.

Critical pre-configuration question: At what level of detail does management need to see costs? If the department heads need to understand their people cost vs. their facilities cost vs. their IT cost, Finance needs cost elements at that level of grouping, not at the individual GL account level.

Cost Object and Element Hierarchies

Both cost objects and cost elements can be organized into hierarchies that drive the rollup structure of cost accounting reports. Cost object hierarchies define how individual cost objects roll up into groups (individual departments roll up into divisions, divisions roll up into business segments). Cost element hierarchies define how individual cost elements roll up into categories for reporting.

Finance designs: The rollup structure Finance uses to produce management reports at different levels of aggregation. A 20-department organization might have departments rolling up to five divisions and the five divisions rolling to the group. The hierarchy determines whether a management report can be produced at any level Finance chooses without separate report definitions for each level.

Critical pre-configuration question: What levels of cost rollup do Finance’s different stakeholder audiences need? The CEO needs the group level; the division head needs the division level; the department head needs the department level. The hierarchy enables all three from the same underlying data.

Allocation Bases and Policies

The mechanisms Finance uses to distribute shared costs from overhead cost objects (shared services, facilities, IT, HR) to the consuming cost objects (the departments, product lines, or customers that benefit from those shared services). The allocation base is the measure Finance uses to determine each consuming object’s share: square footage for facilities costs, headcount for HR costs, ticket volume for IT helpdesk costs, revenue for general overhead.

Finance designs: The allocation policy for each shared cost category: which cost objects are sources (the shared service department), which cost objects are targets (the consuming departments), and what is the allocation basis (the measure that determines each target’s share). Finance also designs the allocation sequence—the order in which allocations run matters when shared service departments consume each other’s services (IT consumes HR, HR consumes IT).

Critical pre-configuration question: Can Finance defend the allocation basis to the department heads who will receive allocated costs? An allocation basis that department heads perceive as arbitrary or unfair produces political resistance to cost accounting output. Finance selects allocation bases that are causally related to cost consumption—not bases that are convenient to measure.

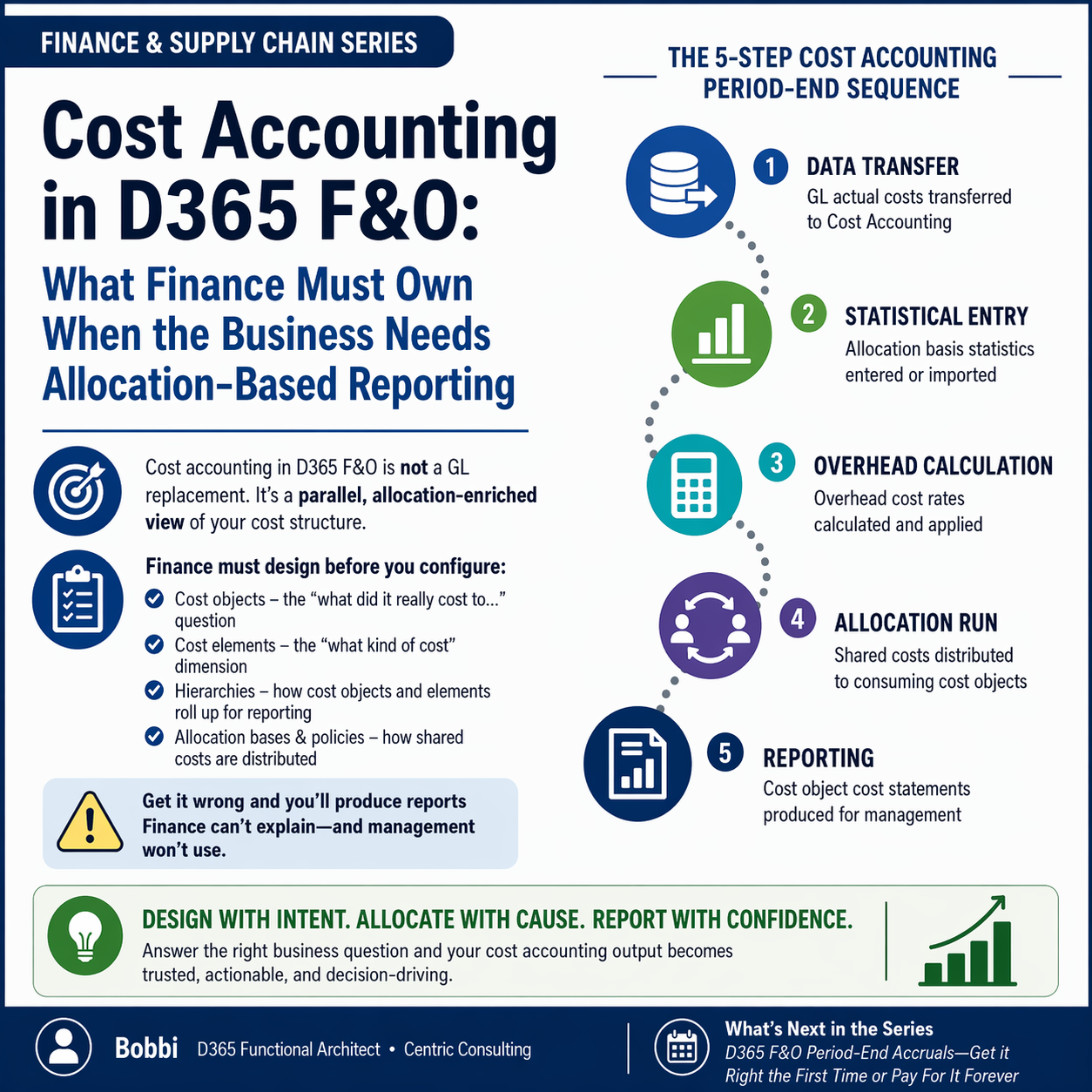

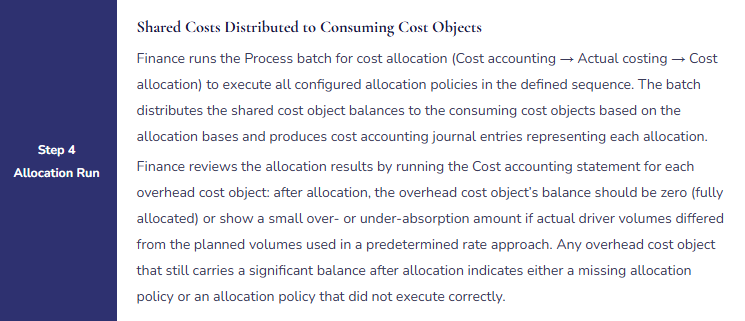

The Allocation Process Finance Must Run at Period End

Cost Accounting Period-End Allocation Sequence—Finance Owns Each Step

Five Cost Accounting Configuration Failures Finance Cannot Explain to Management

⚠️ Cost Accounting Built Without a Defined Business Question—Output Produces Numbers Nobody Uses

Finance implements Cost accounting in D365 F&O because the implementation partner included it in the solution scope. Finance configures cost elements from the GL account structure, creates cost centers as cost objects from the department dimension, and runs allocations using a fixed percentage split that was agreed during implementation. The module runs every month and produces cost center cost statements. The cost center statements are distributed to department heads. After three months, the department heads stop reading them because they cannot understand what the allocated costs mean or why they changed from the prior month. Finance continues running the allocation process and distributing the reports. Nobody acts on them. At the annual implementation review, the CFO asks why the organization is maintaining a cost accounting process that produces reports no stakeholder uses.

Fix: Finance defines the business question Cost accounting is designed to answer before building the architecture: “What does it cost to run each product line including all shared service allocations?” or “What is the full cost per service delivered by each department?” The architecture—cost objects, cost elements, allocation bases—is designed to answer that specific question. Finance also designs the management report that Cost accounting will produce and works backward from that report to confirm the architecture will support it. If Finance cannot articulate the business question and the management report it will produce, Finance is not ready to configure Cost accounting.

⚠️ Allocation Basis Not Causally Related to Cost Consumption—Department Heads Reject the Allocations as Arbitrary

Finance allocates IT costs to departments based on each department’s percentage of total headcount. The IT department’s actual cost driver is IT ticket volume and the number of devices supported per department. The Sales department has 15% of total headcount but generates 45% of IT tickets due to its heavy use of mobile devices and CRM integrations. The Operations department has 35% of headcount but generates 12% of IT tickets because its processes are largely manual. Under the headcount allocation, Sales is allocated 15% of IT costs and Operations is allocated 35%—the inverse of their actual IT consumption. When the Operations Department Head receives her monthly cost statement showing IT costs 2.3x higher than the Sales Department Head’s IT allocation despite having similar technology footprint, she challenges Finance’s methodology. Finance cannot defend the allocation basis and loses credibility with the cost accounting output.

Fix: Finance selects allocation bases that are causally related to cost consumption and can withstand scrutiny from cost object owners. For IT costs: IT ticket count or device count per department. For facilities costs: square footage per department. For HR costs: headcount per department (genuinely causal for HR cost consumption). For training costs: training hours consumed per department. Finance validates the allocation basis selection with the department heads before the first allocation runs—asking whether they consider the proposed basis a fair representation of their consumption of the shared service. Department head buy-in to the allocation methodology is a prerequisite for the cost accounting output to be used for management decisions.

⚠️ Data Transfer Runs Before the Period Is Fully Closed—Cost Accounting Reflects an Incomplete Period

Finance includes the Cost accounting data transfer in the period-close task list, but the task runs on Day +2 before all period-end accruals and adjustments have been posted. The data transfer captures GL entries through Day +2. Post-Day +2 entries—the depreciation batch, the intercompany allocation journals, the period-end accruals for bonuses and provisions—are not in Cost accounting for the period. Department heads receive cost statements that show departmental direct costs but are missing the depreciation allocation, the intercompany service charge, and the bonus accrual. The IT department’s cost statement shows its direct costs at £180,000 when the fully closed period cost including missing entries is £230,000. The department head plans the next month’s spending based on the £180,000 figure, which is materially incorrect.

Fix: The Cost accounting data transfer must run after all period-end entries are posted—it must be the last close task in the sequence, not an early-cycle task. Finance adds the Cost accounting data transfer to the Closing Cockpit as a dependency of the cost object cost statement distribution task, positioned after the fixed asset depreciation batch, all period-end accrual journals, and the intercompany settlement batch have completed and been confirmed. The cost statement distribution to department heads is the final close task—it can only be completed after Finance has confirmed the data transfer captured a fully closed period’s GL entries.

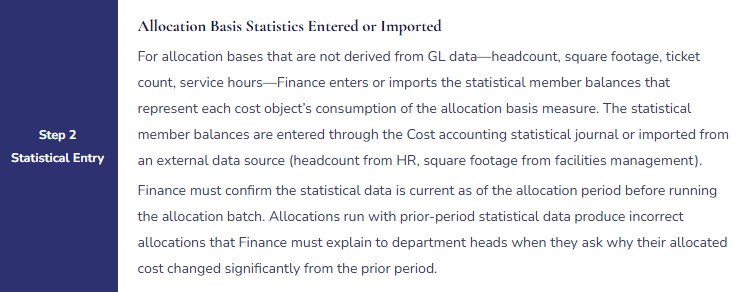

⚠️ Statistical Data Not Updated Before Allocation Run—Allocations Use Six-Month-Old Headcount Data

Finance configured headcount as the allocation basis for HR costs. Headcount data is entered manually as statistical member balances in Cost accounting. When the HR department reorganized and three employees transferred from the Operations division to a newly created Digital transformation division, the headcount statistics in Cost accounting were not updated. For seven months, Cost accounting allocates HR costs based on the pre-reorganization headcount split. Operations is over-charged HR costs for seven employees it no longer has; Digital Transformation is under-charged for seven employees it does have. The cumulative misallocation over seven months is £140,000—Operations is charged £70,000 more than it should be and Digital Transformation £70,000 less. When Finance reconciles the cost accounting output to the actual headcount roster during an annual review, the discrepancy surfaces.

Fix: Finance establishes a statistical data update procedure aligned with the period-end close: before every allocation run, Finance confirms the statistical member balances for all allocation bases are current as of the allocation period. For headcount: Finance receives the headcount by department from HR as of the last day of the period before running the allocation. For square footage: Finance confirms no space changes have occurred with the facilities manager before running the allocation. The statistical data update is a named task in the Closing Cockpit with a specific due date (Day +1, before the allocation batch runs on Day +2) and a specific owner (Finance, not HR or facilities management). Finance is accountable for the accuracy of the allocation inputs, which means Finance must actively obtain and verify the statistical data, not assume it is current.

⚠️ GL Accounts Not Mapped to Cost Elements—25% of GL Cost Is Invisible in Cost Accounting

Finance configures cost element mappings for the GL accounts that represent the main expense categories: salaries, rent, depreciation, utilities, and IT services. Several expense accounts added to the COA after the initial Cost accounting configuration—a new account for environmental compliance costs, an account for ESG reporting expenses, and three accounts added during a financial reporting restructure—were never mapped to cost elements. For eight months, these accounts post costs to the GL that do not transfer to Cost accounting. The cost center statements for departments that use these accounts understate their costs by the amounts charged to unmapped accounts. A cost center that the cost accounting output shows as within budget is in reality significantly over budget when the unmapped costs are included.

Fix: Finance adds “Review Cost accounting cost element mappings for new GL accounts” to the COA change procedure: whenever a new GL expense account is added to the chart of accounts, Finance confirms whether it should be mapped to a cost element in Cost accounting and creates the mapping if it should. Finance also runs a monthly completeness check: compare the total expense charges in the GL for the period to the total costs transferred to Cost accounting. Any difference above materiality indicates an unmapped GL account. Finance investigates the difference and either creates the cost element mapping or explicitly documents that the GL account is intentionally excluded from Cost accounting with a business rationale.

Do This / Don’t Do This

Do This

- Define the specific business question Cost accounting will answer before designing the architecture

- Select allocation bases causally related to cost consumption and validate them with cost object owners before the first allocation run

- Position the Cost accounting data transfer as the last close task in the sequence—after all period-end entries are posted

- Update statistical member balances (headcount, square footage, driver volumes) before every allocation run as a named Closing Cockpit task

- Add “Review Cost element mappings for new GL accounts” to the COA change procedure

- Run a monthly completeness check comparing GL total expenses to Cost accounting total costs transferred

Don’t Do This

- Implement Cost accounting without a defined business question—cost accounting output nobody uses is technical debt with an ongoing monthly maintenance cost

- Use allocation bases that are convenient to measure rather than causally related to cost consumption

- Run the Cost accounting data transfer before the period is fully closed

- Assume statistical data is current without actively confirming it before each allocation run

- Add new GL expense accounts to the COA without reviewing whether they need cost element mappings in Cost accounting

What’s Next:

Cost accounting addresses the internal management reporting layer. The next post returns to the statutory GL and addresses the period-end accounting step Finance performs every close that has more configuration dependency than most Finance teams realize: D365 F&O Period-End Accruals—The Configuration Finance Gets Right the First Time or Pays For Indefinitely—how D365 F&O’s accrual scheme functionality automates recurring period-end accruals, the accrual scheme configuration Finance must build before the first close, the reversal mechanism Finance must understand to avoid double-counting, and the five accrual configuration failures that produce income statement misstatements Finance untangles during audits.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

If a post helped you solve a real problem, share it with a Finance colleague who is in the middle of a D365 Finance and Operations implementation or a post-go-live optimization. If you have a topic the series did not cover, please reach out. There is always one more subject worth exploring.

Interested in learning more? Below are some of my latest posts:

Leave a Reply