How Business Central handles restricted fund accounting, grant budget tracking and spending compliance, donor and grantor reporting, the period-end grant reconciliation Finance must run before releasing grant-funded expenses, and the five grant accounting failures that produce funder audit findings and jeopardize future funding.

The Four Fund Types Finance Must Distinguish in BC

Nonprofit fund accounting requires Finance to track not just how much money the organization has, but whose money it is and what it can be used for. Business Central handles this through the combination of dimensions, G/L account structure, and budget tracking—but Finance must design the configuration to reflect the fund structure, not the other way around.

- Unrestricted Net Assets

- Funds the organization can use for any purpose at the board’s discretion. Operating donations without donor restrictions, earned program revenue, investment returns on unrestricted endowment, and board-designated reserves all fall here. Finance reports on unrestricted net assets as the organization’s financial flexibility measure.

- BC configuration: Unrestricted activity posts to standard operating accounts with no special dimension restriction. The financial statements separate unrestricted net assets from restricted net assets using the BC Financial Reports (Account Schedules) structure.

- Temporarily Restricted Net Assets

- Funds restricted by donors or grantors to a specific purpose or time period. A grant for youth programming, a donor gift restricted to a capital campaign, a government contract for specific services. The restriction releases when the condition is met—the purpose is accomplished or the time period expires.

- BC configuration: Temporarily restricted funds tracked by a dedicated dimension value (e.g., Dimension = Fund, Value = Grant ID or Campaign Code). Budget tracking by fund dimension ensures spending does not exceed the restriction. Restriction release posted via journal entry when the condition is met.

- Permanently Restricted Net Assets

- Endowment principal that must be maintained in perpetuity. The organization can spend the investment income (subject to endowment policy) but not the principal. Finance tracks permanently restricted net assets separately and confirms at every period end that principal has not been invaded.

- BC configuration: Endowment principal tracked in a separate G/L account or set of accounts that Finance restricts from operational posting. Investment income and draws from the endowment use a different account structure that flows to the operating fund.

- Board-Designated Funds

- Funds the board has set aside for a specific purpose from unrestricted net assets—a capital reserve, a technology refresh fund, an operating reserve. These are not donor-restricted; the board can re-designate them. Finance tracks them separately for management reporting even though they are technically unrestricted.

- BC configuration: Board-designated funds tracked by a dimension value or a separate G/L account range, with a budget that represents the board’s authorization. Finance reports on designated fund balances in the management package alongside unrestricted and restricted fund balances.

Configuring BC for Grant Accounting—The Dimension Design Finance Must Own

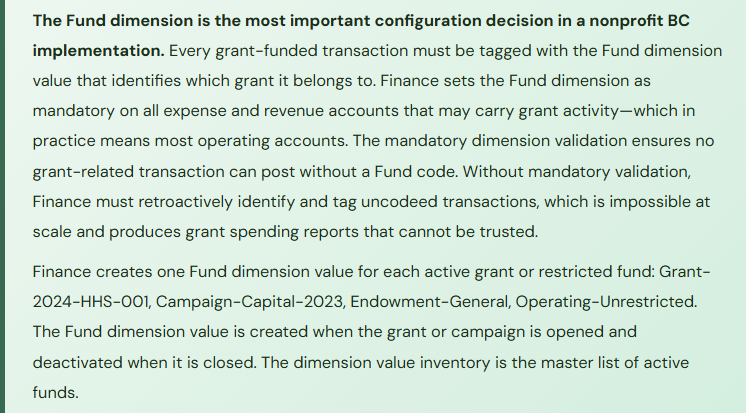

Grant accounting in BC is implemented primarily through BC’s dimension structure. Finance must design the dimensions that support grant tracking before any grant is entered into BC—retrofitting dimension structure after transactions have posted requires retagging historical entries, which is a significant effort and often produces incomplete results.

The standard dimension configuration for nonprofit grant accounting uses two dedicated dimensions: Fund (which grant, campaign, or operating fund this transaction belongs to) and Program (which program or service line the expense or revenue is associated with). For organizations with government contracts that require indirect cost rate tracking, a third dimension for Cost Type (direct vs. indirect) supports the allocation calculations that funders require.

Grant Budget Setup and Spending Compliance in BC

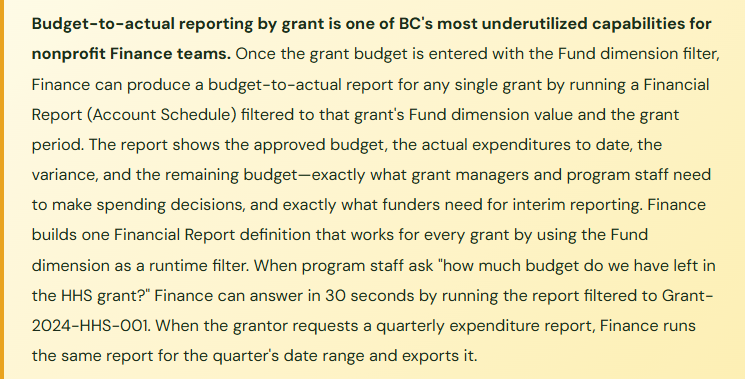

Every grant comes with an approved budget—the amount the grantor has authorized for each spending category over the grant period. Finance must enter this budget into BC and configure BC to provide real-time visibility into spending against each budget line. BC’s budget functionality, filtered by the Fund dimension, provides exactly this capability when configured correctly.

Finance enters the grant budget into BC (Finance → General Ledger → G/L Budgets) with the grant period as the date range, the Fund dimension value as the dimension filter, and budget amounts by G/L account category that mirror the grantor-approved budget categories. The budget entry mirrors the grant agreement’s line-item structure: Personnel, Fringe Benefits, Consultants, Travel, Supplies, Equipment, Indirect Costs (if applicable).

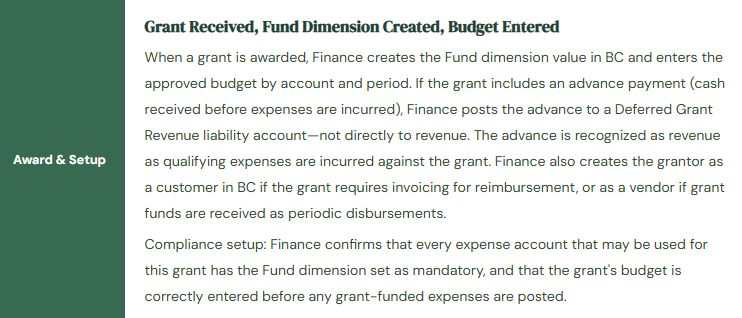

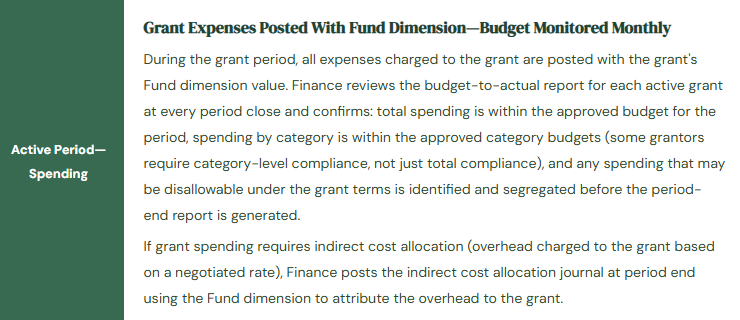

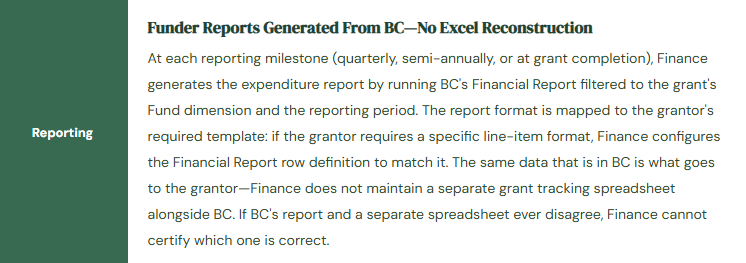

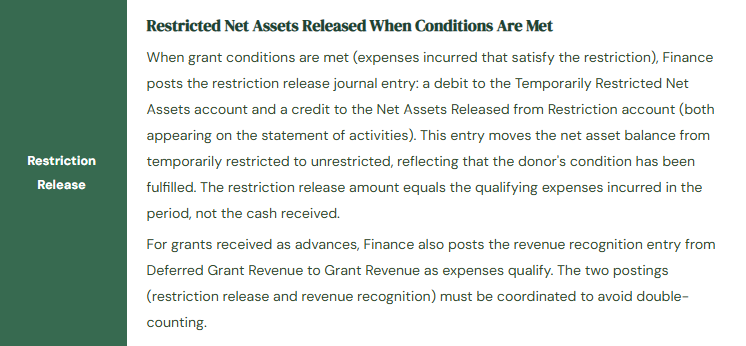

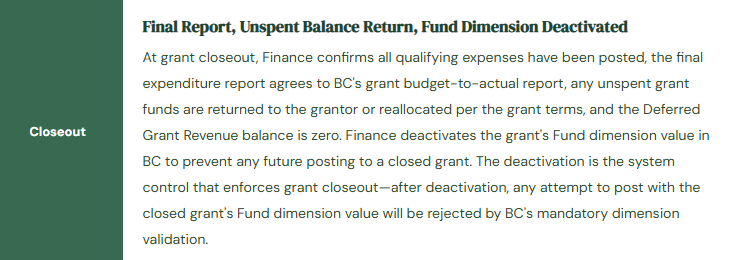

The Grant Lifecycle in BC—Finance-Owned Actions at Each Stage

Grant Lifecycle—Finance Configuration and Posting at Each Stage

Five Grant Accounting Failures That Produce Funder Audit Findings

⚠️ Grant Expenses Posted Without Fund Dimension—20% of Spending Untracked and Unclaimable

The Fund dimension is configured but not set as mandatory on the expense accounts. Over the grant period, 20% of expenses that should have been charged to the government grant are posted without the Fund dimension value—some because the AP coordinator didn’t know the dimension was required, some because the mandatory validation was temporarily disabled to resolve a posting error and never re-enabled. At grant closeout, the budget-to-actual report shows only 80% of the grant’s approved budget spent, with $48,000 of qualifying expenses in the GL that are not tagged to the grant and therefore not visible in the grant report. Finance must manually trace the $48,000 of untagged expenses, confirm they are qualifying expenses under the grant terms, and repost them with the correct Fund dimension. The grantor receives the closeout report late. The corrected report is questioned by the grantor’s auditor, who asks why Finance has corrected postings in the grant period.

Fix: Fund dimension mandatory validation must be enabled and maintained for every expense and revenue account that participates in grant activity. This is not an optional quality improvement—it is the system control that ensures grant tracking is complete. Re-enable mandatory validation immediately if it was disabled as a workaround. The workaround for a posting error is to fix the underlying data or configuration that caused the error—not to disable the control that would have prevented the error from going undetected. Finance confirms mandatory dimension settings are intact on all grant-eligible accounts after every BC update and after any configuration change by running a test transaction against each account category and confirming that a posting without the Fund dimension is rejected.

⚠️ Grant Revenue Recognized at Receipt Rather Than as Expenses Are Incurred

The organization receives a $120,000 government grant payment in April. The AP coordinator who processed the incoming wire transfer debits Cash and credits Grant Revenue for the full $120,000 in April. The grant covers expenses through December. Finance produces the April income statement showing $120,000 of grant revenue—a spectacular April for a program that has not yet incurred the expenses the grant is supposed to fund. The board reviews the April financials and is confused by the revenue spike. The auditors, reviewing the year-end financial statements, identify that grant revenue was recognized on receipt rather than as expenses were incurred—a departure from the generally accepted nonprofit accounting standard for conditional contributions (ASC 958-605). The auditor requires a restatement of the April through December monthly financial statements to spread the revenue recognition across the expense incurrence period.

Fix: Government grants and conditional contributions are not recognized as revenue when received—they are recognized as expenses qualifying under the grant terms are incurred. Finance establishes a grant revenue recognition policy that maps to ASC 958-605 (for US nonprofits) or the applicable accounting standard, and configures BC to enforce it: all grant receipts post to a Deferred Grant Revenue liability account. At each period end, Finance posts the revenue recognition journal to move qualifying expense amounts from Deferred Grant Revenue to Grant Revenue. The revenue recognition amount equals the grant expenses posted in the period that meet the grantor’s conditions. Finance reconciles the Deferred Grant Revenue balance at each period end: the balance should equal the unspent grant funds on hand. If Deferred Grant Revenue is zero but unspent grant cash is in the bank account, Finance has over-recognized revenue.

⚠️ Grant-Funded Personnel Costs Allocated by Estimate—Timesheets Don’t Support the Allocation

The organization’s program director splits her time between three grants and one unrestricted program. Finance allocates her salary 30% to Grant A, 30% to Grant B, 20% to Grant C, and 20% to Unrestricted based on the program director’s initial estimate of her time distribution when the grants were awarded. No timesheets or time records are maintained. Eight months into the grant period, the grantor for Grant A conducts a site audit. The auditor asks for the documentation supporting the 30% salary allocation to Grant A. Finance produces the initial time estimate. The auditor notes that an initial estimate is not sufficient documentation for a salary allocation—the organization must maintain contemporaneous time records (timesheets or equivalent) showing actual time spent on each grant. The grantor disallows $18,000 of the salary charges to Grant A (30% of eight months’ salary) and requires the organization to repay that amount from unrestricted funds.

Fix: Personnel cost allocations to grants require contemporaneous documentation of actual time spent—not estimates, not after-the-fact reconstructions, not percentage allocations entered at the start of the grant period and never updated. Finance establishes a timesheet or effort reporting process for every employee whose salary is charged to a restricted grant. BC’s Jobs or Project module can serve as the timesheet platform for this purpose—employees log time by grant/project code and the logged time drives the payroll cost allocation posted to each grant’s Fund dimension. At a minimum, employees submit monthly effort certifications confirming the percentage of time actually spent on each grant. The certifications are retained as audit documentation. Finance recalculates salary allocations monthly based on actual reported time rather than maintaining a fixed percentage estimate.

⚠️ Unspent Grant Funds Not Returned at Closeout—Organization Retains $22,000 That Belongs to the Grantor

A two-year government grant closes with $22,000 of unspent budget. Finance’s grant closeout procedure involves filing the final report, receiving the grantor’s acceptance, and deactivating the Fund dimension value. Nobody reviews the grant agreement’s provisions for unspent funds. The grant agreement requires that any unspent funds be returned to the grantor within 30 days of grant closeout. Finance does not return the funds because nobody was aware of the provision. Three months after closeout, the grantor’s grants management office contacts Finance requesting the return of unspent funds. Finance must now produce the amount owed, plus potential interest on the retained amount from the due date. The organization’s relationship with the grantor is strained going into the next funding cycle application.

Fix: Grant closeout procedures must include a review of the grant agreement’s unspent fund provisions before the closeout is finalized. Finance maintains a Grant Terms Summary document for each active grant that includes, at minimum: the grant period, the reporting schedule, the indirect cost rate (if applicable), the allowable cost categories, and the unspent fund disposition provisions. This document is reviewed at grant closeout alongside the final budget-to-actual report. If unspent funds must be returned, Finance initiates the return within the required timeframe, posts the return in BC as a deduction from Grant Revenue, and confirms the Deferred Grant Revenue balance is zero after the return. The Grant Terms Summary is prepared when the grant is awarded and maintained as the reference document for all grant compliance questions throughout the grant period.

⚠️ Indirect Cost Rate Not Applied to Grants—Organization Underrecovering Overhead for Three Years

The organization has a negotiated indirect cost rate of 18% on direct salaries for all federal grants. The rate is documented in a rate agreement with the federal cognizant agency. Finance does not configure BC to calculate and post the indirect cost allocation to grant budgets. For three years, every federal grant is charged direct salaries and direct program costs but no indirect costs. The organization is underrecovering $38,000 per year in overhead that it is entitled to charge to federal grants under the negotiated rate. The $38,000 per year in unrecovered overhead is borne by unrestricted operating funds—effectively a subsidy to federal programs that the organization is not required to provide. At the three-year mark, a new CFO reviews the indirect cost rate agreement and discovers the underrecovery. Recovering three years of unrecovered indirect costs requires an amendment to the grant agreements, which the grantor may not approve after the fact.

Fix: If the organization has a negotiated indirect cost rate, that rate must be applied to every eligible grant from the first period of each award. Finance configures the indirect cost allocation in BC as a period-end journal template: the template calculates the indirect cost charge as the negotiated rate applied to the period’s direct salary costs posted to the grant, debits the indirect cost expense account with the grant’s Fund dimension, and credits the indirect cost pool account. The journal is posted monthly as part of the period-close procedure for every active grant with an applicable rate. Finance confirms the total indirect cost recovery against the period’s direct salary costs times the negotiated rate before posting the template. Indirect cost recovery is not optional when a rate agreement exists—it is the mechanism by which the organization recovers its actual overhead costs rather than subsidizing federal programs from unrestricted funds.

Do This / Don’t Do This

Do This

- Design the Fund dimension structure before the first grant transaction is posted—retrofitting dimensions is far more expensive than designing them correctly upfront

- Set Fund dimension as mandatory on all expense and revenue accounts eligible for grant activity

- Post all grant receipts to Deferred Grant Revenue and recognize revenue only as qualifying expenses are incurred

- Enter grant budgets in BC by account category for every active grant before spending begins

- Maintain contemporaneous time records for all personnel whose salary is charged to restricted grants

- Review the grant agreement’s unspent fund provisions as part of every grant closeout procedure

- Apply the negotiated indirect cost rate to every eligible grant from the first period of each award

- Deactivate Fund dimension values at grant closeout to prevent future posting to closed grants

Don’t Do This

- Disable the Fund dimension mandatory validation as a workaround for any posting error

- Recognize grant revenue at cash receipt rather than as expenses are incurred under ASC 958-605

- Allocate personnel costs to grants using initial estimates without contemporaneous time documentation

- Maintain a separate grant tracking spreadsheet alongside BC—the funder report must come from BC or Finance cannot certify its accuracy

- Skip the indirect cost allocation if a negotiated rate exists—underrecovery is a real cost to the organization

- Close out grants without reviewing the unspent fund disposition provisions in the grant agreement

- Leave closed grant Fund dimension values active in BC—they allow future posting to funds that are no longer open

Up Next:

Grant accounting applies to nonprofits and any organization receiving restricted funding. The next post addresses the annual Finance event that affects every BC organization regardless of industry: Preparing Your BC Environment for Audit—the six-week audit preparation timeline Finance must run before external auditors arrive, the BC-specific documentation package that supports the most common audit procedures, the controls evidence Finance must maintain continuously rather than assemble reactively, and the five audit preparation failures that produce extended audit timelines and unnecessary findings.

— Bobbi

D365 Functional Architect · Recovering Controller

Thank you for reading!

If this post helped you solve a real problem, share it with a Finance colleague who is in the middle of an ERP implementation or a post-go-live optimization. If you have a topic that I haven’t covered, please reach out. There is always one more post worth writing.

If you’d like to learn more, below are a few of my latest posts:

Leave a Reply